9-21-20 Weekly Market Update

The very big picture

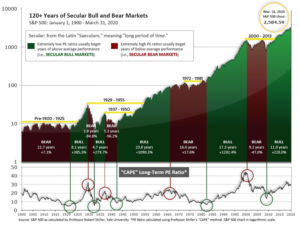

The long-term valuation of the market is commonly measured by the Cyclically Adjusted Price to Earnings ratio, or “CAPE”, which smooths-out shorter-term earnings swings in order to get a longer-term assessment of market valuation. A CAPE level of 30 is considered to be the upper end of the normal range, and the level at which further PE-ratio expansion comes to a halt (meaning that further increases in market prices only occur as a general response to earnings increases, instead of rising “just because”). The market was recently at that level.

Of course, a “mania” could come along and drive prices higher – much higher, even – and for some years to come. Manias occur when valuation no longer seems to matter, and caution is thrown completely to the wind – as buyers rush in to buy first, and ask questions later. Two manias in the last century – the “Roaring Twenties” of the 1920s, and the “Tech Bubble” of the late 1990s – show that the sky is the limit when common sense is overcome by a blind desire to buy. But, of course, the piper must be paid, and the following decade or two were spent in Secular Bear Markets, giving most or all of the mania-gains back.

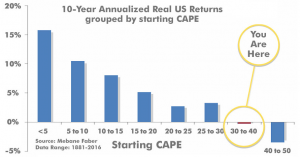

See Fig. 1 for the 100-year view of Secular Bulls and Bears. The CAPE is now at 28.53, down from the prior week’s 30.68. Since 1881, the average annual return for all ten-year periods that began with a CAPE in the 25-35 range have been slightly-positive to slightly-negative (see Fig. 2).

Note: We do not use CAPE as an official input into our methods. However, if history is any guide – and history is typically ‘some’ kind of guide – it’s always good to simply know where we are on the historic continuum, where that may lead, and what sort of expectations one may wish to hold in order to craft an investment strategy that works in any market ‘season’ … whether current one, or one that may be ‘coming soon’!

The Big Picture:

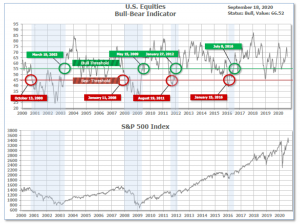

The ‘big picture’ is the (typically) years-long timeframe – the timeframe in which Cyclical Bulls and Bears operate. The U.S. Bull-Bear Indicator is in Cyclical Bull territory at 66.52 down from the prior week’s 69.61.

In the Quarterly- and Shorter-term Pictures

The Quarterly-Trend Indicator based on the combination of U.S. and International Equities trend-statuses at the start of each quarter – was Positive entering July, indicating positive prospects for equities in the third quarter of 2020.

Next, the short-term(weeks to months) Indicator for US Equities turned negative on September 3rd and ended the week at 18, unchanged from the prior week.

In the Markets:

U.S. Markets: U.S. equities finished the week mixed with merger news and renewed COVID-19 vaccine optimism offsetting worries that the Federal Reserve’s monetary policy was becoming less effective in supporting the recovery. The Dow Jones Industrial Average ended the week down just 8 points to 27,657. The technology-heavy NASDAQ Composite fell a steeper -0.6% to 10,793. By market cap, the large cap S&P 500 declined -0.6%, while the mid cap S&P 400 and small cap Russell 2000 gained 0.6% and 2.6%, respectively.

International Markets: Most major international markets were also mixed. Canada’s TSX declined -0.1% along with the UK’s FTSE 100 which gave up -0.4%. France’s CAC 40 and Germany’s DAX finished down -1.1% and ‑0.7%, respectively. Japan’s Nikkei ticked down -0.2%, while China rose 2.4%. As grouped by Morgan Stanley Capital International, developed markets rose 0.5% while emerging markets added 1.3%.

Commodities: Major commodities finished the week to the upside. Oil was the clear winner with West Texas Intermediate crude surging 10.7% and finishing the week at $41.32 per barrel. Precious metals also rose with Gold rising 0.7% to $1962.10 an ounce and Silver gaining 1% to $27.13 per ounce. The industrial metal copper, viewed by some analysts as an indicator of global economic health due to its wide variety of uses, gained 2.5%.

U.S. Economic News: The number of Americans filing first-time unemployment benefits fell last week, but the economy is still suffering from an extreme level of layoffs. The Labor Department reported initial jobless claims fell to 860,000. Economists had expected 870,000 new claims. The decline was the first in five weeks. As a reference, initial claims had been averaging around 200,000 in the weeks leading up to the coronavirus outbreak. Continuing jobless claims, which counts the number of people already receiving benefits, fell by 916,000 to a seasonally-adjusted 12.63 million. That’s the lowest level since April 4th when most of the U.S. economy was shut down.

Home builders are more confident about the state of their industry than ever before, according to research from a builder trade group. The National Association of Home Builders (NAHB) reported its monthly confidence index rose 5 points to 83 this month. The reading was the highest on record in the 35-year history of the data. Robert Dietz, chief economist for the NAHB stated, “The suburban shift for home building is keeping builders busy, supported on the demand side by low interest rates.” Regionally, the Midwest index signaled the biggest increase, rising nine points to 78, followed by the South’s six-point increase to 85. The regional index for the West dropped one point to 87.

Sales at the nation’s retailers climbed in August for the third straight month, the Commerce Department reported. Despite the end of federal aid, U.S. retail sales rose 0.6% last month. Economists were expecting a 0.7% rise. Analysts note the pace of sales has slowed from earlier in the summer, when the economy reopened and many retailers experienced a sharp rebound in customer traffic. Sales gains are likely to be harder to come by in the months ahead, especially after the end of generous federal aid for the unemployed and businesses. Overall retail sales are about 2% higher now compared to pre-pandemic levels in February.

The Federal Reserve revealed its latest outlook on the economy and monetary policy, stating it sees interest rates remaining near zero until the end of 2023. It also reiterated that it intends to keep rates at zero until inflation is on track to exceed 2% for some time and will continue its purchases of Treasuries and mortgage-backed securities. While analysts like Seth Carpenter, economist at UBS, said the Fed guidance was “vague”, Fed Chair Jerome Powell defended the guidance as “powerful” and “durable”. There were two dissents to the Fed forward guidance. Dallas Fed President Rob Kaplan seemed to favor the prior guidance and wanted the Fed to retain greater flexibility once the economy was on track to meet its two goals. Minneapolis Fed President Neel Kashkari proposed a much more streamlined guidance that the Fed would maintain rates close to zero until core inflation has reached 2% on a sustained basis.

Factory activity in the New York region rebounded in September, reversing August’s decline. The New York Federal Reserve reported its Empire State business conditions index rose 13.3 to points to 17. Economists had expected a reading of only 6. This is the third consecutive positive reading in the index. In the details, the new orders index climbed 8.8 points to 7.1, while shipments rose 14.1. Optimism about the six-month outlook rose 6 points to 40.3. The New York index is the first look at manufacturing conditions in September.

The Philadelphia Federal Reserve reported business activity in its region dipped earlier this month. The regional Fed bank’s index fell to 15 from 17.2 in August. This is the index’s fourth consecutive positive reading. Economists had expected a reading of 13. However, analysts note that the components of the index were actually stronger than the headline number. The barometer on new orders rose to 25.5 in September from 19. The shipments index surged to 36.6 in September from 9.4 and the measure of the business outlook for the next six months rose 18 points to 56.6.

Industrial output slowed in August following strong gains earlier in the summer. The Federal Reserve reported U.S. industrial production rose 0.4% last month. The increase followed a 3.5% gain in July and a 6.1% gain in June. Wall Street had expected a 0.5% gain. The index is still 7.3% below its pre-pandemic level in February. Capacity utilization, which measures the percentage of full manufacturing limits of the nation’s factories, mines and utilities, rose to 71.4% in August. Given that the initial rebound following widespread shutdowns appears to be waning some analysts believe growth will be slower through the rest of 2020 and into 2021. Gus Faucher, chief economist of The PNC Financial Group stated, “There were big increases in output in the spring and early summer as factories reopened, but with demand throughout the U.S. and global economies still down substantially from early 2020, it will be more difficult to eke out near-term gains.”

International Economic News: Canada is abandoning free trade negotiations with China amid a host of disagreements on a range of topics. Foreign Minister Francois-Philippe Champagne told reporters, “I do not see the conditions being present now for these discussions to continue at this time. The China of 2020 is not the China of 2016.” The comments mark a major policy shift towards China that brings Canada more in line with the hardline posture adopted by the United States, Australia and parts of the European Union. Relations between Ottawa and Beijing soured after Canadian authorities detained Huawei CFO Meng Wanzhou in 2018 at the request of the US, which was followed by the arrests of two Canadian nationals on charges of espionage in China.

Across the Atlantic, the Bank of England could cut interest rates to below zero next year after officials said preparations were under way to allow the central bank to support the economy with lower borrowing costs. In a move that would bring the BoE into line with the European Central Bank and the Bank of Japan, the monetary policy committee (MPC) said it was seeking to overcome obstacles to negative interest rates that would allow further cuts from the current 0.1% base rate. The MPC said in its September report that the bank was discussing how to overcome technical barriers and put itself in a position to cut rates further, “in light of the decline in global interest rates over a number of years”.

Anger at French President Emmanuel Macron has boiled over, with French trade unions demanding a nationwide strike against the embattled president. The “national days of action” called by the General Confederation of Labour (CGT) and other trade unions followed another factory closure in the country. Japanese tire maker Bridgestone announced this week that it would close its plant in Béthune in northern France with the loss of 863 jobs. There have already been thousands of job cuts across the country from French companies including Airbus, Renault and Sanofi due to economic fallout from the pandemic. In response, around 40,000 workers in France took to the streets on Thursday and Friday for industrial action and to protest against the cuts and low wages.

Economic expectations in Germany continued to rise this month following August’s strong reading. The ZEW economic research institute reported its measure of economic expectations went up to 77.4 in September from 71.5 in August. The outcome exceeded the consensus of 70.0. “Experts continue to expect a noticeable recovery of the German economy,” said Achim Wambach, president of the ZEW institute. Mr. Wambach said stalled Brexit talks and rising Covid-19 cases didn’t dampen the positive mood.

In Asia, the world’s second-largest economy has been in recovery mode for months, and now its consumers are starting to spend even more. China reported its retail sales rose 3.36 trillion yuan ($495 billion) in August, a 0.5% increase over the previous year. While not significant, the gain marks the first year-over-year increase in 2020. “The job market has stabilized, and travel restrictions have loosened,” said Fu Linghui, a spokesman for National Bureau of Statistics. “People are more willing to come out and spend.” China’s recovery makes it an outlier as the pandemic weighs on the rest of the globe.

Japan’s new Prime Minister Yoshihide Suga is expected to pull out all the stops to revive Japan’s economy, continuing the policies of outgoing leader Shinzo Abe, analysts say. Suga was formally voted Prime Minister by parliament’s lower house on Wednesday, and took the helm as Japan’s first new leader in eight years. Abe, who resigned in August due to ill health, is known for his economic policies that are collectively known as “Abenomics.” The three-pronged approach is aimed at combating deflation and reviving economic growth with loose monetary policy and fiscal spending, alongside structural reforms to cope with a rapidly aging population. Suga’s new cabinet roll-out demonstrated his desire to maintain stability and continuity as he kept many ministers in place while choosing new ones from different factions in his Liberal Democratic Party.

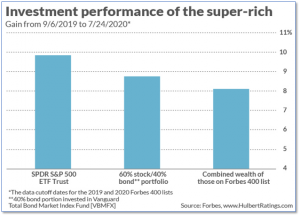

Finally: When thinking of the Forbes 400 list of wealthiest Americans, many would assume that most of the 400 are titans of Wall Street who make money hand over fist through astute investing. But research shows that’s not the case. Mark Hulbert (marketwatch.com) analyzed the investment performance of the super-rich and found that not only did they not beat the benchmark S&P 500, they failed to match the common diversified 60/40 stock and bond portfolio as well. The truth is, almost all the 400 made their money elsewhere and then treat their rather low-risk investing as a way to conserve and keep, rather than grow, their fortunes.

(Sources: All index- and returns-data from Yahoo Finance; news from Reuters, Barron’s, Wall St. Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet.) Securities offered through Registered Representatives of Cambridge Investment Research Inc., a broker-dealer, member FINRA/SIPC. Advisory Services offered through Cambridge Investment Research Advisors, a Registered Investment Adviser. Strategic Investment Partners and Cambridge are not affiliated. Indices mentioned are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results.