6-17-19 Weekly Market Update

The very big picture:

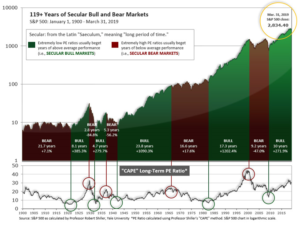

The long-term valuation of the market is commonly measured by the Cyclically Adjusted Price to Earnings ratio, or “CAPE”, which smooths out shorter-term earnings swings in order to get a longer-term assessment of market valuation. A CAPE level of 30 is considered to be the upper end of the normal range, and the level at which further PE-ratio expansion comes to a halt (meaning that increases in market prices only occur in a general response to earnings increases, instead of rising “just because”). The market is currently at that level.

Of course, a “mania” could come along and drive prices higher – much higher, even – and for some years to come. Manias occur when valuation no longer seems to matter, and caution is thrown completely to the wind as buyers rush in to buy first and ask questions later. Two manias in the last century – the 1920’s “Roaring Twenties” and the 1990’s “Tech Bubble” – show that the sky is the limit when common sense is overcome by a blind desire to buy. But, of course, the piper must be paid and the following decade or two are spent in Secular Bear Markets, giving most or all of the mania gains back.

See Fig. 1 for the 100-year view of Secular Bulls and Bears. The CAPE is now at 29.73, up from the prior week’s 29.58, above the level reached at the pre-crash high in October, 2007. Since 1881, the average annual return for all ten year periods that began with a CAPE around this level have been in the 0% – 3%/yr. range. (see Fig. 2).

In the big picture:

The “big picture” is the months-to-years timeframe – the timeframe in which Cyclical Bulls and Bears operate. The U.S. Bull-Bear Indicator (see Fig. 3) is in Cyclical Bull territory at 56.87, up from the prior week’s 55.95.

In the intermediate and Shorter-term picture:

The Shorter-term (weeks to months) Indicator (see Fig. 4) turned positive on June 4th. The indicator ended the week at 14, up from the prior week’s 10. Separately, the Intermediate-term Quarterly Trend Indicator – based on domestic and international stock trend status at the start of each quarter – was positive entering April, indicating positive prospects for equities in the second quarter of 2019.

Timeframe summary:

In the Secular (years to decades) timeframe (Figs. 1 & 2), the long-term valuation of the market is historically too high to sustain rip-roaring multi-year returns. The Bull-Bear Indicator (months to years) remains positive (Fig. 3), indicating a potential uptrend in the longer timeframe. In the intermediate timeframe, the Quarterly Trend Indicator (months to quarters) is positive for Q2, and the shorter (weeks to months) timeframe (Fig. 4) is positive. Therefore, with three indicators positive and none negative, the U.S. equity markets are rated as Positive.

In the markets:

U.S. Markets: U.S. stocks kicked off the week with a strong performance on Monday on news of a trade deal between the U.S. and Mexico but lost some momentum later in the week. The Dow Jones Industrial Average rose 105 points to close at 26,089—a gain of 0.4%. The technology-heavy NASDAQ Composite added 0.7%. By market cap, the large cap S&P 500 index and small cap Russell 2000 index each rose 0.5%, while the S&P 400 mid cap index added 0.4%.

International Markets: Canada’s TSX rose a second consecutive week, gaining 0.4%. The United Kingdom’s FTSE rose 0.2%, while on Europe’s mainland France’s CAC 40 ticked up 0.1% and Germany’s DAX gained 0.4%. In Asia, China’s Shanghai Composite rebounded 1.9% from last week’s decline, while Japan’s Nikkei gained 1.1%. As grouped by Morgan Stanley Capital International, emerging markets declined -0.2%, while developed markets retreated -0.6%.

Commodities: Gold finished a volatile week down a minor -0.1% to $1344.50 an ounce. Silver also finished the week down, but by a more significant -1.5%, to $14.80 an ounce. West Texas Intermediate crude oil retreated ‑2.7% to $52.51 per barrel, its third down week out of the past four. The industrial metal copper, viewed by analysts as an indicator of global economic health due to its wide variety of uses, managed a 0.1% gain—its first positive close in nine weeks.

U.S. Economic News: The number of Americans seeking first-time unemployment benefits edged up to a 5-week high of 222,000, but the overall level remains extremely low. The Labor Department reported that initial jobless claims rose by 3,000 to 222,000 last week. Economists had estimated new claims would total 218,000. The less-volatile monthly average of new claims rose 2,500 to 217,750. The number of people losing their jobs still remains near a half-century low, and far below the 300,000 level analysts use to indicate a “healthy” jobs market. Continuing claims, which count the number of people already collecting unemployment benefits, increased by 2,000 to 1.69 million. That number remains close to a 46-year bottom.

In contrast to a weak Non-Farms Payrolls employment report for May, the Labor Department’s Job Openings and Labor Turnover Survey (JOLTS) reported the total number of workers hired in April rose 240,000 to a new high of 5.9 million—the highest since the Labor Department started keeping track. The total hirings were the most recorded in the data series’ history going back to December 2000. On the openings front, the gap between vacancies and available workers continued to be huge. Openings for the month actually decreased slightly, falling 25,000 to 7.45 million. However, workers that the Bureau of Labor Statistics classifies as unemployed declined by 387,000 to 5.82 million, leaving the gap between available jobs and available workers at 1.63 million.

Sales at the nation’s retailers improved for a third consecutive month as worries of a weakening economy seemingly had no effect. The Commerce Department reported U.S. retail sales increased 0.5% with broad-based gains. Economists had expected a gain of 0.7%. In addition, April’s sales were revised to a 0.3% gain from the initial report of a -0.2% fall. Almost all categories showed solid gains in May. The only declines were food and beverage stores, department stores, miscellaneous stores and clothing. Ian Shepherdson at Pantheon Economics stated, “The consumer is firmly back on track: the first quarter’s softness was misleading.”

Sentiment among the nation’s consumers declined this month, mostly due to tariff concerns. The University of Michigan said its consumer-sentiment index in June fell 2.1 points to 97.9. Economists had expected a reading of 98. A rise in the current conditions component of the index was tempered by a decline in the index of consumer expectations. In the details, the index for expectations over the next 6 months dropped sharply as consumers raised concerns about tariffs (at the time of the survey there was the possibility of tariffs being levied against Mexico). Of note, negative opinions of tariffs were spontaneously made by 40% of surveyed consumers in early June, almost double the percentage from May.

The National Federation of Independent Business (NFIB) reported optimism among small-business owners continued to rise in May, hitting a “historical high”. The NFIB’s index rose 1.5 points to 105.0, exceeding economists’ forecasts of a 102.0 reading. In the details, six of the ten survey components increased, three were unchanged, and only one fell. Nearly two-thirds reported either “hiring” or “trying to hire”, a 5-point increase from April, but over half reported “few or no qualified applicants”—an increase of 5%. In its release, the group said, “It is important to keep policy focus on the small business half of the economy to ensure that it is not dissuaded from investing and hiring because of ‘policy oversight’ – like not making the tax cuts permanent.”

Prices at the wholesale level barely rose according to the latest data from the Bureau of Labor Statistics. The Producer Price Index ticked up just 0.1% in May, matching economists’ forecasts. More notably, the increase in wholesale prices over the past year slowed to 1.8% from 2.2%, down sharply from the 3.1% seen last summer. In the details, the cost of services rose 0.3%, while the cost of goods dropped 0.2%. Wholesale gasoline fell 1.7% and food costs declined 0.3%. Food costs have declined in four of the past five months. Scott Brown, chief economist at Raymond James stated, “The report suggests limited pipeline inflationary pressures. A softer global economy may be putting downward pressure on pipeline inflation in supplies and material, partly offsetting the impact of tariffs.”

Inflation also remained tame at the consumer level. Consumer prices rose just 0.1% in April–its smallest increase in four months. The reading was the smallest increase since January and matched forecasts. In addition, the annual rate of inflation for April fell to 1.8%, down 0.2% from March. Another closely watched measure of inflation that strips out food and energy, the “core rate”, also advanced a meager 0.1% last month. The yearly increase in the core rate slipped to 2% from 2.1% — right in line with the Federal Reserve’s target for inflation.

International Economic News: A recent study found that most Canadian workers are stressed about their pay and stated their employers weren’t transparent enough about how staff are compensated. In an online survey conducted by Hanover Research, 83% of Canadian workers polled said they regularly experience stress related to pay and money problems. In addition, the survey found only 28% of Canadian respondents said they were “completely satisfied” with how transparent their employer is about how staff are compensated. Eddy Ng, a professor of economics and business at Dalhousie University in Halifax, said a shortage of “quality employment” — permanent, full-time jobs — caused by “a structural shift in the economy” is stressing out employees who worry they’ll lose the precarious jobs they do have. Although Canada’s economy has been creating record job growth, those are “not the quality jobs that we have been accustomed to over the last two to three decades,” said Ng.

Britain’s economy contracted sharply in April after auto production had its biggest decline since records began. Earlier in the year, many car manufacturers had announced temporary shutdowns at their British plants, anticipating trade disruption around the time Britain was due to leave the European Union on March 29. However, Prime Minister Theresa May delayed the departure and set a new date of October 31, but it was too late for car makers to change their plans. Britain’s Office for National Statistics stated the economy contracted 0.4% in April, following a 0.1% decline in March. The reading was its biggest decline since March of 2016 and a larger fall than any economist had forecast. Problems went beyond the drop in car production, National Institute of Economic and Social Research economist Garry Young said: “Brexit-related uncertainty at home and trade tensions abroad (are) dragging on investment spending and economic growth.”

The Bank of France maintained its forecast for second-quarter economic growth of just 0.3%, stating growth this year and next will be slightly weaker than anticipated—as will inflation. The country’s central bank attributed the deterioration to a bleak global environment and a smaller-than-expected boost from President Macron’s stimulus. Against the softer economic backdrop and Macron’s tax cuts, the Bank of France added to warnings about France’s public finances. It expects debt as a percentage of GDP to rise in 2019 and then stabilize at around 99% – above the government’s most recent official targets.

The German government stated the country will face sustained economic headwinds in the coming months as global trade tensions hit its export industries and the country’s labor market slows. The German economy ministry stated Germany’s economy grew 0.4% in the first quarter of 2019, in part due to strong consumer spending. However, in its statement the ministry said the outlook for the second quarter “remains muted”. Germany’s reliance on exports makes it particularly vulnerable to turbulence in international trade. Exports of goods and services fell 3.4% month-on-month in April, according to the economics ministry, while imports declined 1.1%.

Economic data on Chinese industrial output and investment released this week added to evidence of a slowdown that some economists said risk breaching the government’s 6% bottom line for growth. The data for May included two key pieces of China’s gross domestic product: value-added industrial production and fixed-asset investment. Industrial production rose 5% from a year earlier, while fixed-asset investment increased 5.6% during the first five months of the year. However, both increases were slower than the prior month’s report. In addition, China’s factory output number was its weakest since 1992. Iris Pang, an economist with ING Bank, said, “China will have to introduce more fiscal stimulus to ensure it can reach the 6% bottom line of growth target this year.”

Japan’s economy is set to contract in the current quarter according to one of the country’s top economic forecasters. Yoshiki Shinke, chief economist at Dai-Ichi Life Research, said in a note that gross domestic product was likely to shrink by 0.5% in the second quarter writing the economy was currently in poor shape despite the expansion at the start of the year. Growth in the first quarter was propped up by falling imports, with consumption and capital spending both hovering around zero, he said. In the current quarter, imports were likely falling with business investment starting to drag on the economy. Shinke’s comments add to economists’ views that Japan’s economy isn’t as healthy as the latest GDP data suggests.

Finally: So what’s the big deal about “inverted interest rates”? Much has been made recently about the “inversion” – when a shorter-term interest rate (typically the 3-month T-Bill yield) exceeds a longer-term interest rate (typically the 10-year Treasury Bond). This is the opposite of the usual relationship, in which longer-term yields are higher simply to compensate for the increased risks embedded in a longer holding period. But why is a rate inversion bad news? The answer can be seen in the graphic below, from Mauldin Economics, which shows that yield inversions have preceded each recession (the gray areas of the chart) for the past 35 years. The San Francisco Fed reports inverted yields have preceded each recession of the last 60 years. So, a big deal indeed!

(Sources: all index return data from Yahoo Finance; Reuters, Barron’s, Wall St Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet) These are the opinions of WE Sherman and Co and not necessarily those of Cambridge, are for informational purposes only, and should not be construed or acted upon as individualized investment advice.

Securities offered through Registered Representatives of Cambridge Investment Research Inc., a broker-dealer, member FINRA/SIPC. Advisory Services offered through Cambridge Investment Research Advisors, a Registered Investment Adviser. Strategic Investment Partners and Cambridge are not affiliated.

Indices mentioned are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results. All Investing involves risk. Depending on the types of investments, there may be varying degrees of risk. Investors should be prepared to bear loss, including total loss of principal.