3-23-20 Weekly Market Update

The very Big Picture

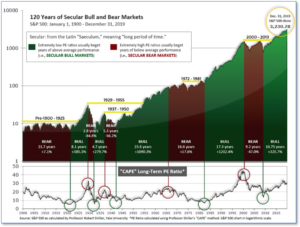

The long-term valuation of the market is commonly measured by the Cyclically Adjusted Price to Earnings ratio, or “CAPE”, which smooths-out shorter-term earnings swings in order to get a longer-term assessment of market valuation. A CAPE level of 30 is considered to be the upper end of the normal range, and the level at which further PE-ratio expansion comes to a halt (meaning that further increases in market prices only occur as a general response to earnings increases, instead of rising “just because”). The market was recently at that level.

Of course, a “mania” could come along and drive prices higher – much higher, even – and for some years to come. Manias occur when valuation no longer seems to matter, and caution is thrown completely to the wind – as buyers rush in to buy first, and ask questions later. Two manias in the last century – the “Roaring Twenties” of the 1920s, and the “Tech Bubble” of the late 1990s – show that the sky is the limit when common sense is overcome by a blind desire to buy. But, of course, the piper must be paid, and the following decade or two were spent in Secular Bear Markets, giving most or all of the mania-gains back.

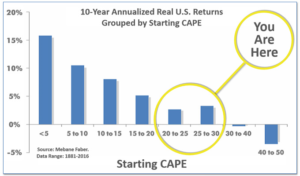

See Fig. 1 for the 100-year view of Secular Bulls and Bears. The CAPE is now at 21.76, sharply down from the prior week’s 25.71 and now well below 30. Since 1881, the average annual return for all ten-year periods that began with a CAPE around the 30 level have been flat to slightly-negative (see Fig. 2).

Note: We do not use CAPE as an official input into our methods. However, if history is any guide – and history is typically ‘some’ kind of guide – it’s always good to simply know where we are on the historic continuum, where that may lead, and what sort of expectations one may wish to hold in order to craft an investment strategy that works in any market ‘season’ … whether current one, or one that may be ‘coming soon’!

The big Picture

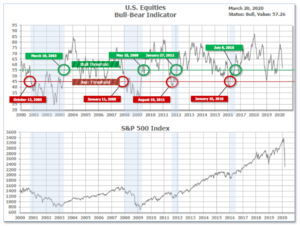

As a reading of our Bull-Bear Indicator for U.S. Equities (comparative measurements over a rolling one-year timeframe), we remain in Cyclical Bull territory. The ‘big picture’ is the (typically) years-long timeframe – the timeframe in which Cyclical Bulls and Bears operate. The U.S. Bull-Bear Indicator (Fig. 1) is in Cyclical Bull territory at 57.26, down from the prior week’s 61.27. The Bull-Bear Indicator is a longer-term indicator that reacts fairly slowly to changes in the market, and cannot make dramatic changes in level over very short periods of time – like the record-setting short period of time of the current decline.

In the Quarterly- and Shorter-term Pictures:

The Quarterly-Trend Indicator based on the combination of U.S. and International Equities trend-statuses at the start of each quarter – was Positive entering January, indicating positive prospects for equities in the first quarter of 2020 as a whole. (On the ‘daily’ version of the Quarterly-Trend Indicator, where the intra-quarter status of the Indicator is subject to occasional change, both the U.S. Equities and International Equities readings remain in ‘Down’ status; the daily International reading turned to Down on Thursday, Feb. 27th; the U.S. daily reading turned to Down on Friday, Feb. 28th.)

Next is the indicator for U.S. Equities, in the shortest time frame. The indicator is Positive at 5, up from the prior week’s 0.

The Complete Picture:

Counting-up of the number of all our indicators that are ‘Up’ for U.S. Equities the current tally is that three of four are Positive, representing a multitude of timeframes (two that can be solely days/weeks, or months+ at a time; another, a quarter at a time; and lastly, the {typically} years-long reading, that being the Cyclical Bull or Bear status).

In the Markets:

U.S. Markets: Stocks suffered another week of steep losses as concerns grew over the impact of the coronavirus pandemic and its effect on major world economies. The S&P 500 index fell back to levels not seen since early 2017, while the Dow Jones Industrial Average touched its lowest levels since late 2016. The downdraft was the most intense on Monday with the Dow suffering its biggest percentage loss since the crash of 1987. The Nasdaq Composite experienced its sharpest daily decline on record. For the week, the Dow Jones Industrial Average plummeted over 4000 points, or -17.3%, ending the week at 19,173. The Nasdaq Composite followed last week’s decline with a further -12.6%. By market cap, the large cap S&P 500 shed -15.0%, while the mid cap S&P 400 and the small cap Russell 2000 finished down -18.7% and -16.2%, respectively.

International Markets: All major international markets finished last week in the red, but most major international markets fared much better than the United States. Canada’s TSX plummeted -13.6%, but the United Kingdom’s FTSE managed a relatively minor ‑3.3% decline. On Europe’s mainland, France’s CAC 40 retreated just -1.7% while Germany’s DAX finished down -3.3%. In Asia, China’s Shanghai Composite gave up -4.9% and Japan’s Nikkei ended down -5.0%. Despite the relatively minor losses in Europe, China and Japan, developed markets as a group finished down -11.1% and emerging markets lost -13.2%.

Commodities: For a second week precious metals failed to live up to their “safe-haven” status. Gold fell -$32.10, or ‑2.1%, to $1484.60 an ounce. Silver plunged -14.6% to just $12.39 an ounce. Crude oil had its fourth week of losses, collapsing -28.7% to $22.63 a barrel for West Texas Intermediate crude oil. Copper, viewed by some analysts as a barometer of global economic health due to its wide variety of industrial uses, finished the week down -11.9%.

U.S. Economic News: The number of Americans applying for first-time unemployment benefits surged last week, as fears over the impact of the coronavirus outbreak triggered layoffs. The Labor Department reported that initial unemployment claims jumped by 70,000 to 281,000 in the week ended March 14. It was one of the biggest one-week increases in history and lifted jobless claims to its highest level since September 2017. Economists had conservatively estimated a forecast of just 220,000. Countless industries are laying off or furloughing employees. Some of the most heavily hit include the airlines, hotels, tourism agencies, retailers, and restaurants. Furthermore, jobless claims are expected to rise much higher in the near future. A flood of new applications this week caused websites in New York and Oregon to seize-up briefly.

Sales of previously-owned homes jumped 6.5% last month, though analysts were quick to point out that the coronavirus outbreak will almost assuredly weigh on growth in the coming months. The National Association of Realtors (NAR) reported existing-home sales occurred at an annualized pace of 5.77 million in February—its strongest reading for the month of February since 2007. The pace of all home sales—both new and existing—was 7.2% higher than the same time a year earlier. In the details, inventory remained tight, which likely limited sales. There was just a 3.1 month supply of homes on the market. Six months is generally considered to indicate a “balanced” housing market. The median sales price for an existing home was $270,100, 8% higher than a year ago. By region, the West had the biggest jump in sales, up 18.9%, while the West and the South also rose. The Northeast saw sales decline 4.1% on a monthly basis, but the volume of sales remained higher than it was a year ago.

In the New York region, business conditions plunged this month according to the New York Federal Reserve. The New York Fed reported its Empire State business conditions index declined a record 34 points to -21.5 this month. Economists had expected a reading of 4.8. The latest reading is its lowest since the financial crisis in 2009. In the details of the report, the new orders index fell the most, down -31.4 points to -9.3, while shipments fell -20.6 points to -1.7. Indicators that track the labor market also weakened. The Empire State business conditions index is one of the first readings that takes into account the coronavirus outbreak’s impact on the economy and the results were alarming. Given that the coronavirus was still in its early stages at the time of this survey, it seems that the worst has yet to come.

It was a similar story from the city of Brotherly Love. The Philadelphia Fed reported its manufacturing index plummeted 49.4 points from positive 36.7 in February to -12.7 by mid-March. That was its lowest reading since June 2012. Economists had expected a reading of 8. Not surprisingly, all the components of the index moved in the same direction – down. New orders fell to -15.5, while the shipments index fell to just 0.2. Oren Klachkin, lead U.S. economist at Oxford Economics summed up the report best stating, “Business conditions in the Philly Fed district look abysmal. It is safe to say that any hope of a manufacturing recovery in 2020 is completely extinguished.”

At the national level, data from the Federal Reserve showed industrial production was strong just before the coronavirus outbreak took hold in America. Industrial production rose 0.6% in February, exceeding analysts’ expectations of just a 0.5% rise. In the details, manufacturing output rose 0.1% led by a 3.5% increase for motor vehicles and parts, however mining output fell 1.5%–a sign of weakness in the energy sector. Capacity utilization rose 0.4% to a very high 77%.

Sales at the nation’s retailers fell last month in what’s likely to become a series of steep declines as the nation slows down. The Commerce Department reported retail sales dropped -0.5% in February. It was the biggest drop in more than a year. Economists had expected an increase of 0.1%. Sales fell the steepest at gas stations, reflecting the plunge in the price of oil, while bars and restaurants posted a decline of 0.5%–a number that will certainly plunge going forward. Several states have ordered restaurants and bars closed, only able to serve takeout, and many more such orders are expected. Internet retailers were the only ones to report a solid increase in sales. Analysts expect retail sales to continue to drop off in the next few months, though they expect supermarkets and internet retailers to weather the storm better than most.

International Economic News: Canada’s Prime Minister Justin Trudeau announced plans to roll out a fiscal stimulus package worth 3% of Canada’s economy as it works to contain the fallout from the coronavirus pandemic. The measures will be worth a combined $56.7 billion USD, Trudeau said. The stimulus is a significant escalation in Canada’s stimulus package and the urgency appears to be ramping up. This week, the price of Canadian heavy crude slumped below $10 a barrel for the first time. “Right now we are focused on making sure that people who are not getting an income or revenue because of this Covid-19 challenge have the money to be able to pay for groceries, pay their rent, and support their families through this difficult time,” Trudeau said. Finance Minister Bill Morneau said the measures were a “first phase” and said the government is prepared to do more if needed.

Across the Atlantic, the United Kingdom announced an unprecedented stimulus plan to cushion the economic blow from the coronavirus, including paying a portion of citizens’ wages for the first time in the nation’s long history. Chancellor of the Exchequer Rishi Sunak stated workers whose jobs are at risk will see up to 80% of their wages paid by the government—potentially costing at least 10 billion pounds ($11.6 billion USD). Companies will also get a 30 billion-pound tax holiday, with the government suspending value-added tax payments for a quarter. JPMorgan Chase & Co. economist Allan Monks stated the measures were “unprecedented” and had an “open-ended or ‘whatever it takes’” rhetoric behind them.

On Europe’s mainland, French President Emmanuel Macron promised that no company will be allowed to fail as a consequence of the disease. The government will guarantee hundreds of billions worth of loans, delay tax payments and suspend rent and utility bills for smaller firms. And the French state is ready to go further, nationalizing industries if necessary. “No French company, whatever its size, will be exposed to the risk of collapse,” President Emmanuel Macron said. The commitment is part of a response that Macron compared to being “at war”.

German Finance Minister has promised $550 billion in loan guarantees and has pledged to provide “unlimited liquidity” to companies affected by the pandemic. The country will also make it easier for companies to access loans made by the state development bank and delay tax payments for struggling businesses. “Due to the high degree of uncertainty in the current situation, the government has very deliberately decided to not set any limits on the volume of these measures,” a German government spokesman said. “If there are any signs of a serious disruption to the economy, the German government … will use all resources available to counter this forcefully.”

In Asia, mainland China has reported zero new domestically transmitted confirmed coronavirus cases for the last two days (if the official numbers are to be believed). Furthermore, other data, both official and third-party appears to confirm that more than 70% of Chinese businesses first affected by the outbreak are now back to work. However, now analysts note that while the storm may have passed China it is just now hitting China’s biggest trading partners. Leland Miller, chief executive officer of China Beige Book noted, “Even if you do see an extraordinary level of domestic resiliency — which I should point out is not yet evident in any of our data — the global spread of Covid-19 has shut down all of China’s major trading partners at just the wrong time.”

Japan’s government is mulling a third round of stimulus measures in an attempt to support its flailing economy. In mid-February the first phase of emergency measures featured 500 billion yen ($4.5 billion) in low-interest, collateral-free emergency loans aimed towards small- to medium-sized businesses in the tourism industry. The second round, announced earlier this month, expanded that support to other virus-hit sectors such as hospitality and manufacturing. The third leg is expected to support the remainder of Japan’s economy affected by the virus—restaurants, hotels, and Japan-based airlines. The Japanese government will lay the groundwork for an additional economic stimulus package after forming a panel of economists and business leaders to help mitigate the economic impact of the coronavirus pandemic. Prime Minister Shinzo Abe said the government’s priority is maintaining employment and business continuity, promising to take “drastic measures to put the Japanese economy back on a steady growth path.”

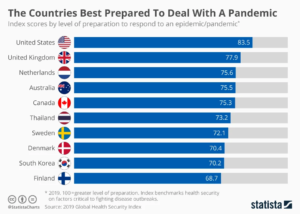

Finally: Critics of the Trump administration’s response to the Covid-19 pandemic have described the preparedness of the U.S. as “pathetic” and “completely inadequate”. But one might ask, “Compared to what?” Well, it turns out that the U.S. was actually better prepared than other nations, whatever you think of that level of preparedness. The Global Health Security Index, a joint project of the Johns Hopkins Center for Health Security and the Nuclear Threat Initiative, ranks countries around the world on their preparedness on a variety of scales and for a variety of health threats. One of them is “Best Prepared to Deal With a Pandemic.” The U.S., shockingly to some, was #1. (chart from statista.com)

(Sources: All index- and returns-data from Yahoo Finance; news from Reuters, Barron’s, Wall St. Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet.) Securities offered through Registered Representatives of Cambridge Investment Research Inc., a broker-dealer, member FINRA/SIPC. Advisory Services offered through Cambridge Investment Research Advisors, a Registered Investment Adviser. Strategic Investment Partners and Cambridge are not affiliated.

Indices mentioned are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results.