3-15-21 Weekly Market Update

The very Big Picture

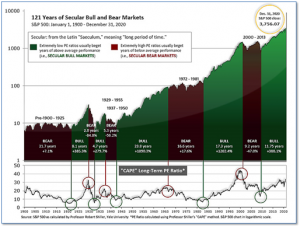

The long-term valuation of the market is commonly measured by the Cyclically Adjusted Price to Earnings ratio, or “CAPE”, which smooths-out shorter-term earnings swings in order to get a longer-term assessment of market valuation. A CAPE level of 30 is considered to be the upper end of the normal range, and the level at which further PE-ratio expansion comes to a halt (meaning that further increases in market prices only occur as a general response to earnings increases, instead of rising “just because”). The market was recently at that level.

Of course, a “mania” could come along and drive prices higher – much higher, even – and for some years to come. Manias occur when valuation no longer seems to matter, and caution is thrown completely to the wind – as buyers rush in to buy first, and ask questions later. Two manias in the last century – the “Roaring Twenties” of the 1920s, and the “Tech Bubble” of the late 1990s – show that the sky is the limit when common sense is overcome by a blind desire to buy. But, of course, the piper must be paid, and the following decade or two were spent in Secular Bear Markets, giving most or all of the mania-gains back.

See Fig. 1 for the 100-year view of Secular Bulls and Bears. The CAPE is now at 35.47, up from the prior week’s 34.79. Since 1881, the average annual return for all ten-year periods that began with a CAPE in the 30-40 range has been slightly negative (see Fig. 2).

Note: We do not use CAPE as an official input into our methods. However, if history is any guide – and history is typically ‘some’ kind of guide – it’s always good to simply know where we are on the historic continuum, where that may lead, and what sort of expectations one may wish to hold in order to craft an investment strategy that works in any market ‘season’ … whether current one, or one that may be ‘coming soon’!

The Big Picture:

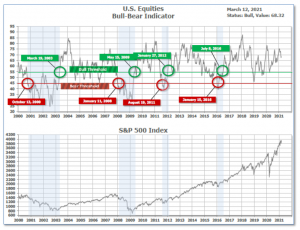

The ‘big picture’ is the (typically) years-long timeframe – the timeframe in which Cyclical Bulls and Bears operate. The U.S. Bull-Bear Indicator is in Cyclical Bull territory at 68.32 up from the prior week’s 67.44.

In the Quarterly- and Shorter-term Pictures

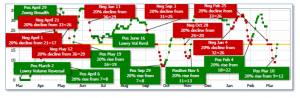

The Quarterly-Trend Indicator based on the combination of U.S. and International Equities trend-statuses at the start of each quarter – was Positive entering January, indicating positive prospects for equities in the first quarter of 2021.

Next, the short-term(weeks to months) Indicator for US Equities turned positive on March 10 and ended the week at 18, up from the prior week’s 11.

In the Markets:

U.S. Markets: U.S. stocks moved broadly higher for the week, lifting most of the major benchmarks to new record highs. The Dow Jones Industrial Average rallied almost a thousand points finishing the week at 32,778, a 4.1% gain. The technology-heavy NASDAQ Composite added 3.1% closing at 13,319. By market cap, the large cap S&P 500 added 2.6%, while the mid-cap S&P 400 and small-cap Russell 2000 rose by 5.3% and 7.3%, respectively.

International Markets: International markets finished the week predominantly to the upside. Canada’s TSX gained 2.6%, while the United Kingdom’s FTSE 100 added 2.0%. On Europe’s mainland, France’s CAC 40 and Germany’s DAX rose by 4.6% and 4.6%, respectively. In Asia, China’s Shanghai Composite fell for a third consecutive week giving up ‑1.4%, while Japan’s Nikkei added 3.0%. As grouped by Morgan Stanley Capital International, developed markets rose 2.2% and emerging markets added 0.3%.

Commodities: In commodities, Gold managed a rebound this week. The precious metal gained $21.30 an ounce finishing the week at $1719.80—an increase of 2.7%. Silver, which is often the more volatile of the two, gained 2.5% to $25.91 per ounce. Oil consolidated after two weeks of gains. West Texas Intermediate crude oil finished down -0.7% to $65.61 per barrel. The industrial metal copper, viewed by some analysts as a barometer of world economic health due to its wide variety of uses, finished the week up 1.6%.

U.S. Economic News: The number of Americans filing for first-time unemployment benefits fell sharply the first week of March to its lowest level since last November. The Department of Labor reported initial jobless claims fell by 42,000 to 712,000 in the week ended March 6. That’s near the lowest level of claims since the pandemic took hold. Economists had expected claims to fall to 725,000. Meanwhile, the number of people already collecting benefits, so-called “continuing claims”, fell by 193,000 to 4.14 million. This is the lowest level of “continuing claims” since last March. Ian Shepherdson, chief economist at Pantheon Macroeconomics believes this is just the start for the improvement in the labor market. In a research note Shepherdson wrote, “A sustained, strong downward trend in claims is just beginning.” He expects claims to fall to 500,000 or less by the end of May.

The number of job openings in the U.S. rose to 6.92 million in January, up from a revised 6.75 million in the previous month the Labor Department reported. Economists had expected job openings to rise to just 6.7 million. In the report, the highest numbers of job openings were in the education, services, and recreation sectors. In addition, the “quits rate”, closely watched because it’s assumed that a workers would only quit a position for a more lucrative one, ticked down to 2.3% in January from 2.4% in the prior month.

The National Federation of Independent Business (NFIB), a small-business lobbying group, found small business owners were more optimistic in February–but the recovery has been uneven. The NFIB reported its index rose 0.8 points to 95.8 in February. The reading fell short of the median forecast of 96.5. In the report, companies said finding enough qualified workers was their biggest problem--even more than taxes or regulatory costs. More than half of the small businesses surveyed said they either hired or tried to hire workers last month, but many could not find suitable workers. Of note, the biggest share of small businesses in 12 years reported they are raising prices–a potential harbinger of coming inflation.

The cost of goods and services at the consumer level rose last month at its fastest pace in 6 months, predominantly due to higher prices at the gas pump. The Bureau of Labor Statistics reported the Consumer Price Index advanced 0.4% in February, matching estimates. The rate of inflation over the past year ticked up to 1.7% from 1.4%. Economists are now expecting inflation to match or exceed its pre-pandemic level of 2.3% by the middle of the year as the U.S. recovery continues to gather momentum. The separate “core” measure of inflation that strips out the often-volatile food and energy categories, edged up a smaller 0.1%. The core rate has increased a more modest 1.3% in the past year, down from 1.4% in the prior month.

Prices moderated at the wholesale level after a big jump in January, but momentum remains to the upside. The Labor Department reported its Producer Price Index (PPI) for final demand rose 0.5% in February. The gain was in line with analysts’ forecasts. Wholesale inflation had jumped 1.3% in January, its biggest gain since 2009. The gain in February was driven by higher prices for energy, which climbed 6%. In the 12 months through February, the PPI accelerated 2.8% after rising 1.7% in the prior month. The core PPI index rose 2.2% over the past 12 months, up 0.2%. Some economists anticipate the recent burst of government spending will cause the economy to overheat. Fed Chairman Jerome Powell has said he thinks the rise in prices will be “temporary”–and that it will take until the summer to know whether this is the case.

International Economic News: Canada saw more economic recovery last month, according to Statistics Canada. In February, Canada’s economy regained almost all of the jobs it lost in the two months prior, and the unemployment rate was at its lowest since March 2020. The number of people employed in February increased by 259,000 after falling by 266,000 in December and January. The number of people working in retail trade as well as accommodation and food services increased in February as coronavirus-related measures were lifted. These industries were among the hardest hit by coronavirus-related closures.

Across the Atlantic, exports from the United Kingdom to the European Union collapsed in January as companies grappled with new terms of trade following the UK’s exit from the EU. The United Kingdom exported goods worth £8.1 billion ($11.3 billion) to the European Union in its first month completely outside the bloc, a 41% decline compared to December, according to the Office for National Statistics. Similarly, imports from the bloc tumbled 29% to £16.2 billion ($22.6 billion) in January compared with the previous month. Kallum Pickering, a senior economist at Berenberg, stated, “While the free trade agreement for goods that the UK and EU signed late last year has mostly brought an end to four and a half years of uncertainty, it does not hold a candle to free trade without paperwork and other non-tariff barriers that the UK once enjoyed as part of the single market.”

On Europe’s mainland, the French economy is on track for 5% growth in 2021, according to the country’s central bank chief. Bank of France governor François Villeroy de Galhau told France Info radio, “The recession is behind us.” French GDP slumped 8.3% in 2020, national statistics bureau Insee estimated in late January, saying that the downturn had turned out to be less brutal than originally forecast. Furthermore, the central bank boss says France will show a level of economic growth well above the European average.

Germany’s IWH economic institute cut its economic growth forecast for this year to 3.7% from 4.4%, as the country now risks a third wave of coronavirus. The Halle-based institute stated, “There is a danger that the steps decided at the beginning of March to open up (the economy) will trigger a third wave of infection. The institute was nonetheless more upbeat about the economy’s prospects this year than the government, which is forecasting 2021 growth of 3%, after a 4.9% slump last year.

In Asia, China’s Premier Li Keqiang said the country’s economic growth target of ‘above 6%’ is not low and leaves room for ‘even faster’ economic expansion. Furthermore, he remarked “This target is not set in stone, it’s intended to guide expectations.” China’s economy grew by 2.3% in 2020, a dramatic turnaround after the coronavirus pandemic ravaged the country in the early part of the year. However, the rebound has been uneven. While major exporters have benefited from a strong rebound in Western countries, many small businesses, which account for the bulk of employment in China, are still struggling to get back on their feet.

Japan confirmed its economy grew by double-digits at the end of last year, according to revised data that continued to show strength in the midst of a resurgence in coronavirus cases. Japan’s Cabinet Office reported gross domestic product grew at an annualized 11.7% from the prior quarter at the end of last year. The figures were slightly weaker than the preliminary estimate of 12.7%. The growth report largely bodes well for the country’s recovery prospects after emergency measures to contain the virus are fully lifted. “The slightly smaller GDP gain doesn’t change the fact that Japan’s economy bounced back robustly,” said Taro Saito, head of economic research at the NLI Research Institute.

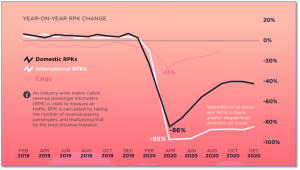

Finally: Air travel plummeted during the dark days of the Spring of 2020, dealing the air travel industry the worst blow since World War II. At the worst, domestic US air travel was down -86%, while international air travel was down -98%. Since then a rebound has taken shape, particularly for domestic US air travel, and at the turn of the year was down “just” 40%. International air travel did not recover nearly to that degree, however, finishing the year still down more than 80% from pre-pandemic levels. Cargo fights, on the other hand, have recovered nearly all the way, and at their worst were down “only” 25%. (Chart from VisualCapitalist.com)

(Sources: All index- and returns-data from Yahoo Finance; news from Reuters, Barron’s, Wall St. Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet.) Securities offered through Registered Representatives of Cambridge Investment Research Inc., a broker-dealer, member FINRA/SIPC. Advisory Services offered through Cambridge Investment Research Advisors, a Registered Investment Adviser. Strategic Investment Partners and Cambridge are not affiliated. Indices mentioned are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results.