1-7-19 Weekly Market Update

The very big picture:

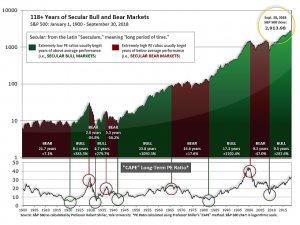

In the “decades” timeframe, the current Secular Bull Market could turn out to be among the shorter Secular Bull markets on record. This is because of the long-term valuation of the market which, after nine years, has reached the upper end of its normal range.

The long-term valuation of the market is commonly measured by the Cyclically Adjusted Price to Earnings ratio, or “CAPE”, which smooths out shorter-term earnings swings in order to get a longer-term assessment of market valuation. A CAPE level of 30 is considered to be the upper end of the normal range, and the level at which further PE-ratio expansion comes to a halt (meaning that increases in market prices only occur in a general response to earnings increases, instead of rising “just because”).

Of course, a “mania” could come along and drive prices higher – much higher, even – and for some years to come. Manias occur when valuation no longer seems to matter, and caution is thrown completely to the wind as buyers rush in to buy first and ask questions later. Two manias in the last century – the 1920’s “Roaring Twenties” and the 1990’s “Tech Bubble” – show that the sky is the limit when common sense is overcome by a blind desire to buy. But, of course, the piper must be paid and the following decade or two are spent in Secular Bear Markets, giving most or all of the mania gains back.

See Fig. 1 for the 100-year view of Secular Bulls and Bears. The CAPE is now at 28.02, up from the prior week’s 27.51, about the level reached at the pre-crash high in October, 2007. Since 1881, the average annual return for all ten year periods that began with a CAPE around this level have been in the 0% – 3%/yr. range. (see Fig. 2).

In the big picture:

The “big picture” is the months-to-years timeframe – the timeframe in which Cyclical Bulls and Bears operate. The U.S. Bull-Bear Indicator (see Fig. 3) is in Cyclical Bull territory at 46.49, up from the prior week’s 46.09.

In the intermediate and Shorter-term picture:

The Shorter-term (weeks to months) Indicator (see Fig. 4) turned positive on November 28th. The indicator ended the week at 7, up sharply from the prior week’s 0. Separately, the Intermediate-term Quarterly Trend Indicator – based on domestic and international stock trend status at the start of each quarter – was negative entering January, indicating negative prospects for equities in the first quarter of 2019.

Timeframe summary:

In the Secular (years to decades) timeframe (Figs. 1 & 2), the long-term valuation of the market is simply too high to sustain rip-roaring multi-year returns. The Bull-Bear Indicator (months to years) remains barely positive (Fig. 3), indicating a potential uptrend in the longer timeframe. In the intermediate timeframe, the Quarterly Trend Indicator (months to quarters) is negative for Q1, and the shorter (weeks to months) timeframe (Fig. 4) is positive. Therefore, with two indicators positive and one negative, the U.S. equity markets are rated as Neutral.

In the markets:

U.S. Markets: U.S. stocks managed a second consecutive week of gains as market weakness midweek gave way to a powerful rally on Friday. The week started off on a positive note, as President Trump tweeted that he and Chinese President Jinping had made “big progress” in trade talks. However, at midweek Apple CEO Tim Cook warned investors that the company was lowering its quarterly revenue guidance – its first such cut in 15 years – triggering a 10% tumble in Apple stock that dragged major indexes sharply lower. The Dow Jones Industrial Average rose 370 points, ending the week at 23,433, a gain of 1.6%. The technology-heavy NASDAQ Composite rose 2.3%. By market cap, the large cap S&P 500 index ended up 1.9%, while the mid cap S&P 400 added 2.3% and small cap Russell 2000 added 3.2%.

International Markets: Canada’s TSX rebounded 1.4% last week, a second week of gains. In Europe, the United Kingdom’s FTSE rose 1.5%, and on Europe’s mainland France’s CAC 40 rose 1.2%, Germany’s DAX gained 2.0%, and Italy’s Milan FTSE added 2.8%. In Asia, China’s Shanghai Composite rose 0.8%, but Japan’s Nikkei finished down -2.3% – its fifth consecutive negative week. As grouped by Morgan Stanley Capital International, developed markets added 2.1%, while emerging markets added 1.2%.

Commodities: Precious metals managed to hold their gains despite the strength in the stock market. Gold finished the week up 0.2% to $1285.80 an ounce. Silver rose a third straight week, gaining 2.3% to $15.79 an ounce. Oil managed a rebound after three weeks of losses, popping 5.8% to $47.96 per barrel. Copper, viewed by some analysts as an indicator of global market health due to its variety of uses, ended the week down -1.3%.

December, Q4 and 2018 Summary:

US stock markets were a sea of red for all three timeframes that concluded in the week ending 12/28/18: the month of December, the 4th Quarter, and the year 2018. On its face, an annual loss of 5% or 6% for the Dow and S&P doesn’t seem so bad, until one remembers that the market was ahead by almost 10% for the year going into October, then gave all that up and then some in a very short time, concluding with the worst December since 1931.

International markets were a sea of even redder red, as all major bourses finished the month, quarter and year in negative territory, and all concluded the year in double negative digits for 2018.

Major commodities also fell for the year 2018, by as much as nearly -25% for “wtic” (West Texas Intermediate Crude). Unlike global stocks, the month of December and the 4th Quarter were mixed, with both gains and losses among the major commodities.

U.S. Economic News: Taking every analyst and expert by surprise, the U.S. economy added 312,000 new jobs in December, blowing away expectations for a gain of just 175,000. The reading brought total employment gains for the year to a three-year high of 2.64 million. Ironically, the strong jobs number actually raised the unemployment rate to 3.9% from a 49-year low of 3.7%, as more Americans entered the workforce in search of jobs. In addition, the Labor Department reported an upwardly-revised 176,000 new jobs were created in November versus the 155,000 originally reported, and October’s gain was also raised to 274,000 from 237,000.

The number of Americans filing new claims last week for unemployment benefits climbed by 10,000 to 231,000. Economists had expected just 220,000 new claims. Jobless claims are often volatile during the holiday season, making them less reliable as an economic indicator at this time of year. Nonetheless, the reading was the third consecutive increase. Overall, however, the reading remained low by historical standards. The four-week average of claims, used by analysts to smooth out the volatility of the weekly number, slipped by 500 to 218,750. Both one-week and the four-week numbers still indicate tight labor market conditions. Continuing claims, which counts the number of people already collecting unemployment benefits, rose by 32,000 to 1.74 million. That reading remains near a 45-year low.

The U.S. added the most private-sector jobs in almost two years, according to private payroll processor ADP. ADP reported employers added 271,000 jobs in December, far above economists’ forecasts who expected a gain of 175,000. It was the highest number of job gains since February of 2017. In the details, small companies added 89,000 jobs, while medium sized businesses added 129,000 and large companies added 54,000.

U.S. manufacturers reported the slowest rate of expansion in 15 months, research firm IHS Markit reported. IHS said its manufacturing Purchasing Managers Index (PMI) dropped 1.5 points to 53.8 in December. It was the fifth decline in the past seven months, and the most since December 2015 as factory activity continued to moderate. New orders and output both grew at their slowest rates in over a year, reflecting softer demand. In addition, payrolls increased at their weakest pace since June 2017. In what could be an ominous sign for the overall economy, the level of optimism among senior executives about the 12-month growth outlook dipped to its lowest level since late fall of 2016. Chris Williamson, chief business economist at IHS Markit stated in the release, “The PMI survey also revealed signs of slower demand growth from customers, as well as rising concerns over the impact of tariffs.”

Separately, the Institute for Supply Management (ISM) reported factory activity grew at a significantly slower pace in December in its monthly survey. The ISM Manufacturing Index plunged 5.2 points in December to 54.1 – its lowest level since November 2016. To put the decline into perspective, it was the biggest decline since October 2008 and a 2.3-standard deviation event. The consensus forecast was for only a mild 1.4-point pullback. In the details, new orders dropped 11.0 points to 51.1—its lowest reading since August of 2016. Production, employment, and inventories also posted slower growth rates. Executives said the ongoing trade war with China and tariffs imposed by both countries have hurt business.

International Economic News: A recent survey of Canadian business executives revealed that optimism is lower than the same time last year as trade issues continue to weigh on sentiment. Research firm RK Insights showed just 30% of survey respondents were optimistic about business prospects for 2019, down from 44% a year earlier. The vast majority, 51%, remained “cautiously optimistic”, while 18% of senior executives were “concerned” about future business prospects. The survey, which was conducted in August and September (prior to the new North American trade deal), showed an increase in concerns about the effects of U.S. President Donald Trump’s trade policies. 65% of survey respondents were “very concerned” about U.S. protectionism – up from 54% the same time last year.

Across the Atlantic, the United Kingdom’s construction sector ended 2018 on weaker footing, hitting a three-year low in December amid fading demand for commercial projects. According to Markit/Cips, the UK’s Purchasing Managers’ Index (PMI) dropped 0.6 point to 52.8, missing economists’ forecasts. The latest reading showed construction companies weakened the final month of 2018 as new orders grew at a more subdued pace. Tim Moore, the economics associate director at IHS Markit stated, “Subdued domestic economic conditions and an intense headwind from political uncertainty resulted in the weakest upturn in commercial work for seven months.”

After six weeks of riots, French police have arrested a prominent leader of the “Gilets Jaunes” (yellow-vest) protests that have rocked the nation’s capital and other French cities. Eric Drouet, a 33-year old truck driver from the Paris suburbs, was one of the original organizers of the movement and was arrested and charged with “organizing an undeclared demonstration”. French law requires that organizers of street demonstrations must inform the local authorities about their plans. Violators face six months of jail and a fine of about 7,500 euros ($8500). French President Emmanuel Macron sparked the protests after instituting a steep fuel tax to ostensibly combat climate change.

Germany’s manufacturing sector showed further signs of slowing, according to Markit’s latest Purchasing Managers’ Index (PMI). Germany’s manufacturing PMI declined 0.3 point to 51.5, a 33-month low. The number is inching closer to the 50-level, the line of demarcation between growth and contraction. December’s reading was the eleventh time in 2018 that the manufacturing index fell, implying sustained weakness in Europe’s economic powerhouse. Germany was hit particularly hard by the ‘dieselgate’ scandal in which millions of German-built diesel cars were found to be fitted with “defeat devices” which could identify when they were being emissions tested. Phil Smith, principal economist at IHS Markit stated, “The darkening global economic picture has had ramifications for Germany’s outwardly focused manufacturing sector over the course of 2018, while the sequence of headwinds in the car industry in the latter stages of the year has been a further restricting factor.”

Despite an agreement between U.S. President Donald Trump and Chinese President Xi Jinping not to apply new levies during a 90-day negotiation period, there are plenty of signs that China’s growth is slowing. A government-led think tank, the Chinese Academy of Social Sciences, recently cut its growth estimate for China’s economy from 6.5% this year to 6.3%. Although it seems like a small difference, when multiplied over the country’s 1.4 billion inhabitants it signifies a dramatic drop in consumer spending. Coresight Research reported retail sales in China grew 8.1% in November over the prior year—its slowest rate of growth in 15 years. In addition, citing data from the National Bureau of Statistics in China, they reported export growth plummeted to just 5.4% in November, down from 15.5% in October. Apple CEO Tim Cook laid the blame for Apple’s lower first-quarter revenue projection on China’s slowing economy, sparking a steep market sell-off on Thursday.

Recent Japanese data revealed that industrial output contracted in November and retail sales slowed sharply. The Ministry of Economy, Trade, and Industry reported factory output declined 1.1% in November, predominantly due to a pullback in production of general purpose machinery. And although the figure was better than the median market forecast of a -1.9% decline, the outlook pointed to a -0.8% decline in January as well. Takeshi Minami at Norinchukin Research Institute stated, “Factory output is in a trend towards leveling off. Japan’s export-reliant economy will face a severe situation next year due to the US-China trade frictions and their ripple effects just as global trade growth is decelerating.” Adding to concerns about overseas demand, Japan’s private consumption, which accounts for about 60% of the economy, showed no signs of strength either. Japan’s retail sales rose just 1.4% year-to-date in November, a sharp slowdown from the 3.6% increase seen in October, and far below the 2.2% gain expected by economists.

Finally: Back in 1965, Martha and the Vandellas sang “Nowhere to run, baby, nowhere to hide”.

That was true as well in 2018, at least in the world of investing. The graphic below, from visualcapitalist.com, shows just how tough the investing environment of 2018 was.

Bonds were flat, the US dollar was modestly higher…and that was it. Non-US stocks fared much worse than US stocks, and the near-universal prediction that Emerging Markets would be the best bet for 2018 was a complete bust as Emerging Markets were the worst of worldwide equity indexes.

(sources: all index return data from Yahoo Finance; Reuters, Barron’s, Wall St Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet) These are the opinions of WE Sherman and Co and not necessarily those of Cambridge, are for informational purposes only, and should not be construed or acted upon as individualized investment advice.

Securities offered through Registered Representatives of Cambridge Investment Research Inc., a broker-dealer, member FINRA/SIPC. Advisory Services offered through Cambridge Investment Research Advisors, a Registered Investment Adviser. Strategic Investment Partners and Cambridge are not affiliated.

Indices mentioned are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results. All Investing involves risk. Depending on the types of investments, there may be varying degrees of risk. Investors should be prepared to bear loss, including total loss of principal.