1-22-2018 Market Update

1-22-2018 Market Update

The very big picture:

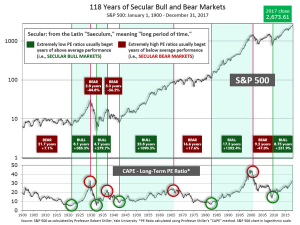

In the “decades” timeframe, the current Secular Bull Market could turn out to be among the shorter Secular Bull markets on record. This is because of the long-term valuation of the market which, after only eight years, has reached the upper end of its normal range.

The long-term valuation of the market is commonly measured by the Cyclically Adjusted Price to Earnings ratio, or “CAPE”, which smooths out shorter-term earnings swings in order to get a longer-term assessment of market valuation. A CAPE level of 30 is considered to be the upper end of the normal range, and the level at which further PE-ratio expansion comes to a halt (meaning that increases in market prices only occur in a general response to earnings increases, instead of rising “just because”).

Of course, a “mania” could come along and drive prices higher – much higher, even – and for some years to come. Manias occur when valuation no longer seems to matter, and caution is thrown completely to the wind as buyers rush in to buy first and ask questions later. Two manias in the last century – the 1920’s “Roaring Twenties” and the 1990’s “Tech Bubble” – show that the sky is the limit when common sense is overcome by a blind desire to buy. But, of course, the piper must be paid and the following decade or two are spent in Secular Bear Markets, giving most or all of the mania gains back.

See Fig. 1 for the 100-year view of Secular Bulls and Bears. The CAPE is now at 33.90, up from the prior week’s 33.80, and exceeds the level reached at the pre-crash high in October 2007. This value is at the lower end of the “mania” range. Since 1881, the average annual return for all ten year periods that began with a CAPE around this level has been in the 0% – 3%/yr. range. (see Fig. 2).

In the big picture:

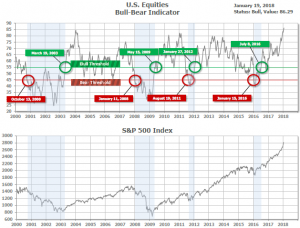

The “big picture” is the months-to-years timeframe – the timeframe in which Cyclical Bulls and Bears operate. The U.S. Bull-Bear Indicator (see Fig. 3) is in Cyclical Bull territory at 86.29, up from the prior week’s 85.00.

In the intermediate and Shorter-term picture:

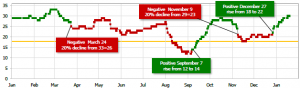

The Shorter-term (weeks to months) Indicator (see Fig. 4) turned positive on December 27th. The indicator ended the week at 30, up from the prior week’s 29. Separately, the Intermediate-term Quarterly Trend Indicator – based on domestic and international stock trend status at the start of each quarter – was positive entering January, indicating positive prospects for equities in the first quarter of 2018.

Timeframe summary:

In the Secular (years to decades) timeframe (Figs. 1 & 2), the long-term valuation of the market is simply too high to sustain rip-roaring multi-year returns – but the market has entered the low end of the “mania” range, and all bets are off in a mania. The only thing certain in a mania is that it will end badly…someday. The Bull-Bear Indicator (months to years) is positive (Fig. 3), indicating a potential uptrend in the longer timeframe. In the intermediate timeframe, the Quarterly Trend Indicator (months to quarters) is positive for Q1, and the shorter (weeks to months) timeframe (Fig. 4) is also positive. Therefore, with internal unanimity expressed by all three indicators being positive, the U.S. equity markets are rated as Positive.

In the markets:

U.S. Markets: The major U.S. equity markets finished the holiday-shortened week with modest gains, with all the major indexes also hitting all-time highs. The Dow Jones Industrial Average rose 268 points to close at 26,071, a gain of 1.04%. The technology-heavy NASDAQ Composite added 75 points to end the week at 7,336, also a 1.04% gain. By market cap, large caps continued to show relative strength over their smaller brethren. The large-cap S&P 500 added 0.86%, while the mid-cap S&P 400 rose 0.67% and the Russell 2000 gained just 0.36%.

International Markets: Canada’s TSX reversed last week’s decline by rising 0.28%. In the United Kingdom, the FTSE retreated -0.6%. On Europe’s mainland, major markets finished in the green with France’s CAC 40 rising 0.2%, and Germany’s DAX and Italy’s Milan FTSE each adding 1.4%. In Asia, China’s Shanghai Composite gained 1.7%, Hong Kong’s Hang Seng surged 2.7%, and Japan’s Nikkei rose 0.7%. As grouped by Morgan Stanley Capital International, emerging markets rose 1.9%, while developed markets added 0.9%.

Commodities: Precious metals lost a bit of their luster as gold retreated -0.13% to close at $1,333.10 an ounce, and silver fell a larger -0.6% to $17.04 an ounce. Energy also retreated. Brent crude oil fell -1.75% to $68.65 a barrel, along with West Texas Intermediate crude oil which slipped -1.5% to $63.31 per barrel. The industrial metal copper, used by some analysts an indicator of global economic health due to its variety of uses, fell -1%.

U.S. Economic News: According to the Labor Department, the number of Americans seeking new unemployment benefits plunged by 41,000, its biggest one-week decline since 2009. In addition, the total number of initial claims was just 220,000—its lowest level since February 1973. Economists had forecast claims would fall only slightly to 250,000. The less-volatile monthly average of new claims declined a lesser 6,250 to 244,500. Initial jobless claims have remained under the key 300,000 threshold for 150 consecutive weeks, the longest stretch since 1967. Joshua Shapiro, chief U.S. economist at MFR Inc. stated, “The role of claims as a leading indicator of the unemployment rate remains intact and the signal is for further declines in the jobless rate.” Continuing claims, which counts the number of people already receiving unemployment benefits, rose by 76,000 to 1.95 million.

Confidence waned among the nation’s homebuilders, but overall sentiment remained positive. The National Association of Home Builders (NAHB) sentiment index dropped two points this month but remained near its highest levels in 18 years. In the details, each of the index’s three sub-gauges retreated. Current sales conditions and future sales each fell a point, while buyer traffic fell four points, but all sub-gauges remained above 50 signaling improving conditions. As has been a common theme for months, the NAHB cited the rising price of building materials and lots, and shortages of skilled labor as the biggest concerns among its members.

The Commerce Department reported that new home construction fell 8.2% last month to a 1.19 million annual rate, missing economists’ forecasts for a reading of 1.28 million. In the details, single-family home starts were down 11.8%, while construction on buildings with five or more units, such as apartment buildings, rose 2.6%. Home construction in all four of the nation’s regions fell. The South led with a 14.2% drop, followed by a 4.2% decline in the Northeast. Permits, which are used as an indicator of future home building activity, remained essentially flat at 1.3 million. The final numbers for 2017 showed that it was a very good year overall, with permits, housing starts, and the number of new homes completed all hitting their highest levels since 2007.

Sentiment among the nation’s consumers fell this month to its worst reading since July, according to the University of Michigan. The University of Michigan’s consumer sentiment index fell to 94.4, missing economists’ expectations for a reading of 98. In the details, consumers reported their current conditions as worsening while they were a bit more optimistic about the future. The report stated “less attractive pricing” for goods and services was the reason for the concern. Consumers remained somewhat confident about future buying plans, thinking the tax cuts will help them to some extent. Tax reform was mentioned by 34% of respondents, with 70% believing the impact would be positive and 18% saying it would be negative. The survey’s chief economist Richard Curtin stated, “The disconnect between the uncertain future outlook assessment and the largely positive view of the tax reform is due to uncertainties about the delayed impact of the tax reforms on the consumers. Some of the uncertainty is related to how much a cut or an increase people, especially those in high-income households living in high-tax states, face.”

The Federal Reserve’s latest ‘Beige Book’—a collection of anecdotes describing the current economic conditions in each of its districts, showed a relatively subdued response to the Republican tax plan. In the report that covered late November to early January, the Federal Reserve said the pace of growth continues to be “modest to moderate.” Most districts reported “on-going labor market tightness and challenges finding qualified workers across skills and sectors.” In some instances, the lack of workers was constraining growth. The report stated that the outlook for this year “remains optimistic for a majority of contacts across the country.” The report comes two weeks ahead of the Fed’s next rate-setting committee meeting, at which it is widely expected to hold short-term interest rates steady.

International Economic News: The Bank of Canada hiked its benchmark interest rate to 1.25%, its third increase since last summer. The central bank pointed to unexpectedly solid economic numbers as the key driver behind the decision. The bank also indicated that the economy will likely need an even higher benchmark over time. However, it also noted that it will remain cautious when considering future hikes by assessing incoming data such as the economy’s sensitivity and reaction to the higher borrowing rates. In its statement, the bank said, “Recent data have been strong, inflation is close to target, and the economy is operating roughly at capacity.” The rate increase by the Bank of Canada is expected to prompt Canada’s large banks to raise their prime lending rates, a move that will drive up the cost of variable-rate mortgages and other variable-interest rate loans.

The United Kingdom the Office for National Statistics reported that inflation in the UK has fallen for the first time since June—dipping to 3% (annualized) last month. The reading was a tick down from the 3.1% level set in November, which was a six-year high. The ONS acknowledged that it was too early to tell whether the decline was the start of a longer-term reduction in the rate of inflation. Separately, the Bank of England said that it believed inflation peaked at the end of last year and should fall back to its target of 2% this year. The rate had been rising over the past year, partly due to the fall in the value of the British pound since the time of the Brexit vote, which has pushed up the cost of imported goods.

On Europe’s mainland, French Finance Minister Bruno Le Maire presented an upbeat view of France’s economic performance over the past year. According to Le Maire, France is likely to have exceeded its initial growth forecast and grown by 2% last year. Le Maire told business leaders that growth was solid and that 2018 should be even better than its forecasts. Last week, the Bank of France upgraded its estimate of growth in 2017 to 1.9% on the heels of strong economic data in the fourth quarter. Le Maire stated that business morale is at its highest level in 10 years and more than 250,000 jobs were added to the retail sector. However, Le Maire warned against becoming too optimistic. “Clarity demands that we recognize that daily life remains difficult for millions of French people, who are facing unemployment and poverty,” he said.

Germany again defended itself from criticism from the International Monetary Fund and Europe over its economic surplus. Germany has been criticized for not using its budget surplus to make further investments which could help other troubled Eurozone economies. Jens Weidmann, president of the German central bank responded stating, “Raising public spending in order to reduce Germany’s current account surplus would be a futile undertaking.” Based on macro-economic simulations, even if Germany were to increase its public investment by 1% of GDP over a two-year period, the models showed it would have a “very small” impact on other euro economies. In addition, the Bundesbank president noted that while Germany has been prudent to reach its current economic health, it must remain prudent due to demographic risks. Germany has an aging population that will increase its costs for healthcare and pensions.

China reported its fastest economic growth in seven years, stating its gross domestic product grew by 6.9% in 2017. The reading beat Beijing’s official annual expansion target of 6.5%. In its release, the National Bureau of Statistics stated, “The economy has achieved stable and healthy development.” The report noted the value of Chinese exports grew by nearly 11% from the previous year, while the combined value of imports and exports rose by 14.2%. China’s trade surplus stands at near $447 billion. As the second-largest economy in the world, China’s is now about two-thirds the size of the United States – and gaining fast.

The Japanese government upgraded its assessment of the economy for the first time in seven months according to Japan’s Cabinet Office. In its monthly report, the Cabinet Office stated, “The Japanese economy is recovering at a moderate pace”, a slightly more optimistic phrase than the one used in December, according to analysts. The wording of the report makes it more likely that the government will confirm that the economy is in its second-longest postwar expansion cycle. A Cabinet Office official stated, “With consumption picking up, improvements have been spreading (beyond the corporate sector) to households. This led to the upward revision.” Hiroshi Miyazaki, senior economist at Mitsubishi UFJ Morgan Stanley Securities stated, “The outlook for the global economy is good, and that influences things like Japan’s exports. In addition, there are no domestic factors that suggest Japan’s growth will falter.”

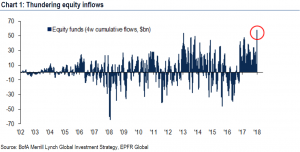

Finally: As the market continues to hit new highs, investment giant Merrill Lynch (ML) released a note to clients that investors are piling into equities in a big way. Per ML’s chief investment strategist Michael Hartnett, “FOMO”, or the “Fear of Missing Out”, has triggered a massive inflow into global equity funds over the last week and month. At $23.9 billion, it was the seventh largest weekly equity inflow on record and led to the highest monthly inflow of $58 billion on record.

(sources: all index return data from Yahoo Finance; Reuters, Barron’s, Wall St Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet)

Indices mentioned are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results. All Investing involves risk. Depending on the types of investments, there may be varying degrees of risk. Investors should be prepared to bear loss, including total loss of principal.