5-28-18 Market Update

5-28-18 Market Update

The very big picture:

In the “decades” timeframe, the current Secular Bull Market could turn out to be among the shorter Secular Bull markets on record. This is because of the long-term valuation of the market which, after only eight years, has reached the upper end of its normal range.

The long-term valuation of the market is commonly measured by the Cyclically Adjusted Price to Earnings ratio, or “CAPE”, which smooths out shorter-term earnings swings in order to get a longer-term assessment of market valuation. A CAPE level of 30 is considered to be the upper end of the normal range, and the level at which further PE-ratio expansion comes to a halt (meaning that increases in market prices only occur in a general response to earnings increases, instead of rising “just because”).

Of course, a “mania” could come along and drive prices higher – much higher, even – and for some years to come. Manias occur when valuation no longer seems to matter, and caution is thrown completely to the wind as buyers rush in to buy first and ask questions later. Two manias in the last century – the 1920’s “Roaring Twenties” and the 1990’s “Tech Bubble” – show that the sky is the limit when common sense is overcome by a blind desire to buy. But, of course, the piper must be paid and the following decade or two are spent in Secular Bear Markets, giving most or all of the mania gains back.

See Fig. 1 for the 100-year view of Secular Bulls and Bears. The CAPE is now at 32.34, up slightly from the prior week’s 32.24, and still exceeds the level reached at the pre-crash high in October, 2007. This value is in the lower end of the “mania” range. Since 1881, the average annual return for all ten year periods that began with a CAPE around this level have been in the 0% – 3%/yr. range. (see Fig. 2).

In the big picture:

The “big picture” is the months-to-years timeframe – the timeframe in which Cyclical Bulls and Bears operate. The U.S. Bull-Bear Indicator (see Fig. 3) is in Cyclical Bull territory at 68.41, up from the prior week’s 67.49.

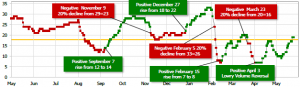

In the intermediate and Shorter-term picture:

The Shorter-term (weeks to months) Indicator (see Fig. 4) turned positive on April 3rd. The indicator ended the week at 19, up from the prior week’s 16. Separately, the Intermediate-term Quarterly Trend Indicator – based on domestic and international stock trend status at the start of each quarter – was negative entering April, indicating poor prospects for equities in the second quarter of 2018.

Timeframe summary:

In the Secular (years to decades) timeframe (Figs. 1 & 2), the long-term valuation of the market is simply too high to sustain rip-roaring multi-year returns – but the market has entered the low end of the “mania” range, and all bets are off in a mania. The only thing certain in a mania is that it will end badly…someday. The Bull-Bear Indicator (months to years) is positive (Fig. 3), indicating a potential uptrend in the longer timeframe. In the intermediate timeframe, the Quarterly Trend Indicator (months to quarters) is negative for Q2, and the shorter (weeks to months) timeframe (Fig. 4) is positive. Therefore, with two indicators positive and one negative, the U.S. equity markets are rated as Neutral.

In the markets:

U.S. Markets: The major U.S. market indexes finished the week flat to slightly higher in light trading ahead of the long holiday weekend. The Dow Jones Industrial Average edged up 38 points, ending the week at 24,753, a gain of 0.2%. The technology-heavy NASDAQ Composite added 1.1%, closing at 7,433. Large caps outperformed smaller caps with the large cap S&P 500 gaining 0.3% for the week, while the mid cap S&P 400 added 0.2% and the small cap Russell 2000 ending up just 0.02%.

International Markets: Canada’s TSX gave up half of last week’s gain by falling -0.5%. Across the Atlantic, the United Kingdom’s FTSE also reversed last week’s gain, retreating -0.6%. On Europe’s mainland, markets were red across the board. France’s CAC 40 ended down -1.3%, while Germany’s DAX and Italy’s Milan FTSE gave up -1.1% and -4.5%, respectively. China’s Shanghai Composite retreated -1.6% alongside Japan’s Nikkei which fell -2.1%. As grouped by Morgan Stanley Capital International, emerging markets rose 0.8% while developed markets were off -1.6%.

Commodities: Precious metals regained some of their luster with Gold rising 1%, or $12.40, to end the week at $1303.70 an ounce. Silver, likewise, ended up 0.6% closing at $16.55. In energy, crude oil plunged on news that OPEC was planning to increase production as early as June to prevent further price increases from weighing on demand. West Texas Intermediate crude oil fell -4.9% to $67.88 a barrel, while North Sea Brent crude oil was off -2.6% to $76.45. Copper, viewed by some analysts as an indicator of global economic health due to its variety of industrial uses, finished the week up 0.5%.

U.S. Economic News: The number of people seeking new unemployment benefits rose to a 7-week high, but analysts were quick to point out that the increase is probably tied to seasonal swings in education-related employment such as cafeteria workers and bus drivers. The Labor Department reported that initial jobless claims rose by 11,000 to 234,000 last week, exceeding economists’ forecasts of a reading of 219,000. The less-volatile monthly average of new claims rose by 6,250 to 219,750. The nationwide unemployment rate remains at an extremely low 3.9%. Continuing claims, which counts the number of people already receiving unemployment benefits, increased by 29,000 to 1.74 million. That number is reported with a one-week delay.

Sales of newly-constructed homes slipped in April, down 1.5% from March but still up 11.6% from the same time last year. The Commerce Department reported new homes were at a 662,000 selling pace, missing economists’ estimates of 682,000. Year-to-date sales are 8.4% higher than in the same period in 2017. The median sales price of a new home last month was $312,400—0.4% higher than a year ago. The slightly slower sales pace caused the available inventory to creep up. There is currently a 5.4 months’ supply of homes available on the market, still below the 6 months generally considered to be a balanced housing market.

Sales of existing homes dropped more than expected in April, as a shortage of property available for sale continued to weigh on the market. The National Association of Realtors (NAR) reported existing home sales fell 2.5% to a seasonally-adjusted annual rate of 5.46 million homes last month. Last month’s decline was the first in three months. Year-on-year, existing home sales were down 1.4%. By region, sales were down the most in the Northeast which saw a decline of 4.4%. In the South, sales were down 2.9% and in the West they were down 3.3%. The Midwest region was unchanged. At April’s sales pace, it would take 4.0 months to clear the current inventory, down from 4.2 months a year ago. The median house price increased 5.3 percent from one year ago to $257,900 in April. It marked the 74th straight month of year-on-year price gains.

A measure of U.S. economic activity from the Chicago Federal Reserve ticked up last month as a stronger performance from factories and a robust labor market helped offset slight weakness in the housing market. The Chicago Fed’s National Activity Index was a positive 0.34 in April, up from 0.32 in March. The index’s less-volatile three-month moving average registered a positive 0.23 last month, up from 0.11. Production-related indicators, which measures manufacturing and factory activity, contributed a positive 0.27 to the index, up from 0.19 in March. Employment-related indicators added 0.10. Of note, the contribution of personal consumption and housing was negative 0.05 in April. The Chicago Fed’s National Activity index is a weighted average of 85 economic indicators, designed so that zero represents trend growth and a three-month average below -0.70 indicates a recession has begun.

Orders for goods designed to last at least three years, so-called ‘durable goods’, fell 1.7% last month, but the decline was almost entirely due to a drop in contracts for Boeing airplanes. Stripping out the outsized effects of planes and cars, orders minus transportation was actually up 0.9%, marking its third consecutive month of gains. In the details, orders for commercial jets plunged 29% in April, following a 61% spike in March. Aside from that gyration, orders for most durable goods rose. In a positive sign for the future, orders for core capital goods rose 1% last month and are up almost 7% in the past 12 months. That’s an indication that companies have stepped up their spending for equipment after several years of weak investment.

Along with the Chicago Fed’s index, research firm IHS Markit reported its flash U.S. Manufacturing Purchasing Managers index (PMI) ticked up 0.1 point to 56.6 this month, touching its highest level since September of 2014. The data showed strong gains in manufacturing production and new business, with signs that manufacturers intend to boost production schedules in the near future. In the services sector, where most Americans are employed, the PMI specifically for services also increased. IHS Markit’s flash U.S. services PMI climbed 0.9 point to 55.7 last month. That reading is at a three-month high. There was a slight slowdown in new business but the backlog of work was the highest since March of 2015. Of note, inflation pressures were evident in the data with input costs measured across both manufacturing and services sectors rising at their fastest rate in nearly five years.

Sentiment among the nation’s consumers came in weaker than expected in the final reading for May. The University of Michigan’s survey of consumer attitudes dipped to 98.0 from 98.8, missing economists’ expectations of a 98.9 reading. Richard Curtin, chief economist of the survey, said in a statement, “The May survey, however, found that consumers anticipated smaller income gains than a month or year ago, even though they anticipate the unemployment rate to stabilize at its current 18-year low.” Overall, Americans remain optimistic about the economy. Incomes are rising, job openings are at a record high, and layoffs and unemployment are at their lowest levels in decades. The index measures 500 consumers’ attitudes on future economic prospects, in areas such as personal finances, inflation, unemployment, government policies and interest rates.

Minutes from the latest Federal Reserve Open Market Committee meeting revealed support for a rate hike in June and that the committee was not concerned about inflation pressures at the moment. The minutes stated, “Most participants judged that if incoming information broadly confirmed their economic outlook, it would likely soon be appropriate for the FOMC to take another step in removing policy accommodation.” Although inflation hit the Fed’s 2% target in its latest reading in March, officials were not convinced it would remain there for long. “It was noted that it was premature to conclude that inflation would remain at levels around 2%, especially after several years in which inflation had persistently run below the Fed’s 2% objective,” the minutes said. Only a “few” officials thought inflation might move “slightly” above the 2% target. Traders in the federal funds futures market see more than a 90% chance of a June rate hike.

International Economic News: The Bank of Canada has highlighted rising household debt and imbalances in the real estate market as the two chief vulnerabilities in the Canadian financial system in the event of a recession. And analysts note that the housing market itself may be the trigger for the next recession. In most developed economies the housing market is the lynch pin that binds together the construction, finance, insurance, and real estate sectors of the economy. Tighter mortgage rules and higher interest rates have weighed on Canada’s once high-flying real estate market, with home sales in Toronto having their worst start to the year since 2009. Still, analyst David Doyle of Macquarie Capital Markets notes, roughly half of all economic weakness during recessions since the Second World War is tied to fluctuations in residential investment, he calculates, and the extent to which Canadian output and employment are currently reliant on this single sector is “unprecedented.”

The United Kingdom’s economy just posted its worst quarterly GDP figures for the last five years according to the UK’s Office for National Statistics. The ONS reported weak household spending and falling levels of business investment dragged the economy down to a 0.1% growth rate in the first quarter. Rob Kent-Smith of the ONS said: “Overall, the economy performed poorly in the first quarter, with manufacturing growth slowing and weak consumer-facing services.” In the details, the figures show the services industries contributed the most to GDP growth, with an increase of 0.3% in the first quarter, while household spending grew at a meagre 0.2%. The construction industry declined by 2.7% and business investment fell by 0.2%.

Thousands of protestors took to the streets in Paris after French labor unions, left-wing political parties, and civil rights groups called for “floods of people” to oppose the economic policies of President Emmanuel Macron. Philippe Martinez, head of leading French union CGT, advised the president to “look out the window of his palace to see real life.” Marches and rallies also were held in dozens of other French cities as part of the joint action against Macron’s policies that organizers consider pro-business and “harsh”. The protestors allege that Macron supports tax reforms that favor the wealthy and obstruct public services. Macron nonetheless asserted that his economic changes are meant to increase France’s global competitiveness and that “No disorder will stop me, and calm will return.”

Recent data from the Munich-based Ifo Economic Institute showed confidence among Germany’s business leaders held steady in May, suggesting company executives in Europe’s economic powerhouse are keeping their cool despite the possibility of a global trade war. Ifo’s business climate index held steady at 102.2, beating the consensus forecast for a reading of 102.0. Klaus Wohlrabe an economist at Ifo said the domestic economy, particularly the trade, construction, and services sectors, had been largely responsible for the stabilization. “The downward trend has stopped,” he added. “The global economic environment is difficult, but the German economy is holding its ground.” However, Andreas Scheuerle, economist at DekaBank, disagreed, contending the trend had not yet changed and stated: “The news that is currently raining down on companies really does not lend itself to creating a positive mood.”

In a move seen as a significant step toward easing the current trade tensions between the U.S. and China, Chinese authorities are set to approve Qualcomm’s planned acquisition of NXP Semiconductors. Chinese regulators have expressed concerns that the merged company would crowd out domestic businesses in areas such as mobile payments. China’s State Administration for Market Regulation, which has been conducting the antitrust review, is expected to approve the merger, removing the last major hurdle for the deal that has been stuck for months amid U.S.-China trade tensions. China had been holding up reviews of multibillion-dollar takeovers as leverage as Beijing seeks to fend off the Trump administration’s trade offensives.

By several measures, the economy of Japan appears to be booming. Total activity is now 1.5% above normal capacity, unemployment is at just 2.5%, and businesses’ spare capacity is at its lowest levels since 1993. In all 47 prefectures, there is more than one job opening for every active job seeker. But a mystery still remains: where is the inflation? Masatsugu Asakawa, vice-minister of finance laments, “Almost every indicator has been great. The only mystery is the weak performance of prices.” Inflation in the year through April was just 0.4% when fresh food and energy are excluded. That’s better than the outright deflation that generally prevailed from 1998 to 2012, but not by much, and it’s way below the Bank of Japan’s 2% target. While steady prices may sound like a good thing, with inflation at or below 0%, interest rates also get stuck at 0%, and the central bank’s ability to stimulate the economy by cutting rates is effectively nullified.

Finally: The U.S. Census Bureau reports that from 1978 through 2015 the median size of a single-family home in America increased every year until it peaked at 2,467 square feet in 2016. But does the average family really need such a big house? Steve Adcock, author of the Get Rich Slowly blog, notes that in reality—it’s largely a big waste of space. A research team affiliated with UCLA studied American families and where they spend most of their time while inside their homes.

The results are quite interesting. As the graphic (source: UCLA) shows, most of the square footage is unused as people tend to gather around the kitchen and television, leaving the dining room, living room, music room and porch mostly or completely ignored. Adcock notes “The findings were not pretty. In fact, they helped prove how little we use our big homes for things other than clutter.”

(sources: all index return data from Yahoo Finance; Reuters, Barron’s, Wall St Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet)

Indices mentioned are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results. All Investing involves risk. Depending on the types of investments, there may be varying degrees of risk. Investors should be prepared to bear loss, including total loss of principal.