4-30-18 Market Update

4-30-2018 Market Update

The very big picture:

In the “decades” timeframe, the current Secular Bull Market could turn out to be among the shorter Secular Bull markets on record. This is because of the long-term valuation of the market which, after only eight years, has reached the upper end of its normal range.

The long-term valuation of the market is commonly measured by the Cyclically Adjusted Price to Earnings ratio, or “CAPE”, which smooths out shorter-term earnings swings in order to get a longer-term assessment of market valuation. A CAPE level of 30 is considered to be the upper end of the normal range, and the level at which further PE-ratio expansion comes to a halt (meaning that increases in market prices only occur in a general response to earnings increases, instead of rising “just because”).

Of course, a “mania” could come along and drive prices higher – much higher, even – and for some years to come. Manias occur when valuation no longer seems to matter, and caution is thrown completely to the wind as buyers rush in to buy first and ask questions later. Two manias in the last century – the 1920’s “Roaring Twenties” and the 1990’s “Tech Bubble” – show that the sky is the limit when common sense is overcome by a blind desire to buy. But, of course, the piper must be paid and the following decade or two are spent in Secular Bear Markets, giving most or all of the mania gains back.

See Fig. 1 for the 100-year view of Secular Bulls and Bears. The CAPE is now at 31.73, virtually unchanged from the prior week’s 31.74, and still exceeds the level reached at the pre-crash high in October, 2007. This value is in the lower end of the “mania” range. Since 1881, the average annual return for all ten year periods that began with a CAPE around this level have been in the 0% – 3%/yr. range. (see Fig. 2).

In the big picture:

The “big picture” is the months-to-years timeframe – the timeframe in which Cyclical Bulls and Bears operate. The U.S. Bull-Bear Indicator (see Fig. 3) is in Cyclical Bull territory at 65.78, down slightly from the prior week’s 65.82.

In the intermediate and Shorter-term picture:

The Shorter-term (weeks to months) Indicator (see Fig. 4) turned positive on April 3rd. The indicator ended the week at 13, down from the prior week’s 17. Separately, the Intermediate-term Quarterly Trend Indicator – based on domestic and international stock trend status at the start of each quarter – was negative entering April, indicating poor prospects for equities in the second quarter of 2018.

Timeframe summary:

In the Secular (years to decades) timeframe (Figs. 1 & 2), the long-term valuation of the market is simply too high to sustain rip-roaring multi-year returns – but the market has entered the low end of the “mania” range, and all bets are off in a mania. The only thing certain in a mania is that it will end badly…someday. The Bull-Bear Indicator (months to years) is positive (Fig. 3), indicating a potential uptrend in the longer timeframe. In the intermediate timeframe, the Quarterly Trend Indicator (months to quarters) is negative for Q2, and the shorter (weeks to months) timeframe (Fig. 4) is positive. Therefore, with two indicators positive and one negative, the U.S. equity markets are rated as Neutral.

In the markets:

U.S. Markets: The major U.S. indexes finished the week flat to modestly lower as the busiest earnings week of the season came to a close. This week, 168 of the companies in the S&P 500 – representing 42% of its market capitalization – reported first-quarter profits. The Dow Jones Industrial Average reversed last week’s gain falling ‑151 points to close at 24,311, a loss of -0.6%. The technology-heavy NASDAQ Composite finished the week down -0.4%, closing at 7,119. By market cap, large caps fared the best. The S&P 400 mid cap index fell ‑0.4% and the Russell 2000 small cap index retreated ‑0.5%, while the large cap S&P 500 index ticked down just ‑0.01%.

International Markets: Canada’s TSX followed last week’s gain with an additional 1.2% rise. The United Kingdom’s FTSE 100 also had a strong week, rising 1.8%. On Europe’s mainland, major markets also finished the week in the green. France’s CAC 40 rose 1.3%, Germany’s DAX added 0.3%, and Italy’s Milan FTSE gained 0.4%. In Asia, China’s Shanghai Composite added 0.4% and Japan’s Nikkei gained 1.4%. As grouped by Morgan Stanley Capital International, emerging markets finished the week flat, while developed markets were off -0.1%.

Commodities: Precious metals ended down for the second week. Gold ended the week at $1323.40 an ounce, down ‑1.1%. Silver fell a much steeper ‑3.9%, closing at $16.50 an ounce. In energy, West Texas Intermediate crude oil had its first down week in three, giving up -0.44% and ending the week at $68.10 a barrel. Copper, seen by some analysts as an indicator of global economic health due to its wide variety of uses, finished the week down ‑2.8%.

U.S. Economic News: The number of Americans seeking new unemployment benefits fell to their lowest level since 1969 last week, the latest indication that the roaring labor market is showing no signs of slowing. The Labor Department reported Initial Jobless Claims fell by 24,000 to 209,000 last week, far below economists’ forecasts of a 230,000 reading. The less-volatile monthly average of new claims declined by 2,250 to 229,250. Continuing claims, which counts the number of people already receiving benefits, dropped by 29,000 to 1.84 million. Overall, the jobs market can be summed up as “excellent”. Practically all workers who want a job can find one and companies are still hiring at a rapid pace. Companies’ biggest complaint continues to be a shortage of skilled workers to fill needed roles.

Sales of existing homes continued to rise despite a worsening supply crunch, according to the National Association of Realtors (NAR). Last month existing-home sales were at a 5.60 million seasonally-adjusted annual pace, up 1.1% from February but still down 1.2% from the same time last year. The median sales price for a home sold in March was $250,400, up 5.8% compared to a year ago. Homes were on the market for an average of just 30 days, bringing the available supply of homes down to a very low 3.6 months of inventory. Six months of inventory is generally considered a healthy housing market. Sales were very mixed by region. In the Northeast, sales surged 6.3% and in the Midwest sales rose 5.7%. In the West, sales dropped 3.1% and in the South, sales ticked down 0.4%.

Supporting the NAR’s report of rising home prices, the S&P/Case-Shiller national home price index for February rose a seasonally-adjusted 0.5%. On an annualized basis, home prices nationwide are up 6.3% from the same time last year. With the more narrowly-focused 20-city index, it took 12 years but prices regained their bubble-era peak, rising a seasonally-adjusted 0.8%. The 20-city index is up 6.8% from a year ago, its strongest reading since mid-2014. Lean supply and outsized demand are keeping home prices booming. No cities experienced monthly price declines in February.

Sales of new homes surged to a four-month high last month, running at a seasonally-adjusted annual rate of 694,000, the Commerce Department reported. The reading trounced economists’ forecasts of a 630,000 annual rate and was at its highest level since November. The government is reporting a 5.2 month supply of new homes on the market, with the median sales price up 4.8% compared to the same time last year. The government’s residential construction data is often volatile and subject to large revisions, nonetheless the data shows a housing market grinding slowly and steadily higher. David Berson, chief economist for Nationwide wrote in a note, “It is likely that the lack of supply of existing homes, and the resulting stagnant pace of sales in that sector, is pushing home buyers into the new-home sales market.”

Economic activity across the nation cooled last month according to the latest reading of the Chicago Fed’s National Activity Index. The National Activity Index retreated from a multi-year high reached in February, weighed down by slower hiring in a still-robust job market. The index was a positive 0.10 in March after reaching a positive 0.98 in February. The less-volatile three-month moving average of the index was 0.18. February’s reading was the highest for the index since October of 1999. The Chicago Fed index is a weighted average of 85 economic indicators designed so that zero represents trend growth and a three month average below negative -0.70 suggests a recession has begun. Of the 85 individual indicators, forty-four made positive contributions, while 41 weighed.

Orders for goods expected to last at least three years, so-called ‘durable goods’, jumped 2.6% last month (mostly due to a large order for Boeing airplanes). The Commerce Department reported that the reading exceeded economists’ expectations of a 2.5% increase. Stripping out the volatile transportation sector (i.e., Boeing), orders were unchanged for the month. Of concern, business investment fell for the third time in four months based on orders for core capital goods, which dipped 0.1%.

Research firm IHS Markit reported American companies in the manufacturing and services sectors grew last month in a reflection of the steadily expanding U.S. economy. In manufacturing, IHS Markit’s flash U.S. Manufacturing Purchasing Managers’ Index (PMI) rose 1 point to 56.5, touching a three-and-a-half year high. A similar survey of service-oriented businesses also rose, edging up 0.4 points to 54.4. Flash readings are based on approximately 85-90% of total responses each month, with the final readings coming later. Chris Williamson, chief business economist at IHS Markit stated, “After a relatively disappointing start to the year, the second quarter should prove a lot more encouraging.”

Confidence among the nation’s consumers rebounded in April with a small gain that put the index back near an 18-year high. The Conference Board reported the Consumer Confidence Index climbed to 128.7 this month, up 1.7 points from March. In the details of the report, the present situation index, which measures consumers’ feelings of current conditions, rose to 159.6 from 158.1. The future expectations index advanced 1.9 points to 108.1. Americans were more optimistic about their own finances and felt that jobs were easy to find, the survey showed. Lynn Franco, director of economic indicators at the board stated, “Overall, confidence levels remain strong and suggest that the economy will continue expanding at a solid pace in the months ahead.”

Gross Domestic Product for the first quarter grew a solid 2.3% as businesses stepped in to fill the gap left by consumers. The U.S. economy expanded in the first three months of the year, as business investment doubled to 12.3%, while consumer spending rose just 1.1%–its smallest increase in almost five years. Analysts believe consumers took a break on spending to pay off their bills and rebuild their savings following a robust holiday season. Severe bouts of bad weather may also have hampered spending. Businesses picked up the slack, however, with business investment and spending on equipment both rising sharply. The biggest corporate tax cuts in 30 years are believed to have helped give a lift to investment in the first quarter.

International Economic News: Louis Vachon, head of the National Bank of Canada, states that the Canada has a permit problem—and its hurting the economy. Vachon stated the Canadian economy is splitting into two extremes, a “permit economy” where resource and manufacturing companies face delays and roadblocks for project approvals, and a booming service and technology economy. Vachon notes that the export numbers generated by the “permit economy” are well below potential along with private investment in those sectors. However the service industry is doing “extremely well”, Vachon said. “That’s why the major urban areas are booming and the startup scene is really accelerating in Canada.”

Britain’s economy suffered its weakest growth in over 5 years, growing by just 0.1% in the first quarter of 2018. The reading was well below the Bank of England’s prediction of 0.3% and at the bottom end of economists’ forecasts. The low reading essentially ended the chances of a rate hike next month. Year-over-year, growth slowed to 1.2%, down from 1.4% the previous quarter. The BoE’s Monetary Policy Committee (MPC) begins meetings next week on whether to raise rates on May 10 for only the second time since the 2008 financial crisis. John Wraith, market strategist at UBS noted, “For us, it means no hike at all in 2018.” Scotiabank economist Alan Clarke stated, “If the MPC wants to look through this number and hike they can justify it – they just have a challenge selling it to the man and woman on the street.”

Despite President Emmanuel Macron’s pro-business push, growth in France also decelerated sharply in the first quarter. French national statistics agency INSEE estimated first quarter growth at 0.3%, down -0.4% from the previous quarter. The agency attributed the decline to a fall in household consumption after five consecutive quarters of growth of above 0.5% growth. Household spending only rose 0.2% in the first three months of the year, while growth in company investment dropped -1.1% to just 0.5%–despite ex-banker Macron’s campaign to make France more business friendly. Many French economists had expected a dip in first quarter GDP and don’t expect it to impact overall growth for the year. Mathieu Plane of the OFCE economic observatory at Sciences Po University stated, “The slowdown in growth is not a sign of a reversal in the economic situation or the end of a cycle. The underlying conditions are still good.”

Morale among German businesses dropped again this month according to research firm Ifo’s German business climate index. The index fell 1.2 points this month to 102.1, marking its fifth consecutive month of declines. Economists said the results pointed to a mixed picture for the German economy, a key pillar of the Eurozone’s economic health. Carsen Brzeski, chief economist of Germany at ING wrote a note to clients stating, “Today’s disappointing reading will feed the discussion on whether Germany and the entire euro zone is currently only in a soft patch or actually at the start of an unexpected downswing.” Joerg Kraemer, chief economist at Commerzbank, said that the survey pointed to a slowdown in growth momentum while Claus Vistesen, chief euro zone economist at Pantheon

Macroeconomics, said the results, in two words, were “nicht gut” (not good).

China’s leaders are signaling that growth in the world’s second-largest economy could slow due to trade and financial risks, and they’re prepared to adjust policy to avoid a sharp deceleration. Following a Politburo meeting last week, state media reported that hard work is needed to meet this year’s economic targets amid an “increasingly complicated geopolitical situation.” Though growth remained robust in the first quarter, analysts still see the economy slowing this year as trade tensions with the US and the campaign to clean up the financial sector remain as downside factors. The Politburo statement mentioned the need to boost domestic demand for the first time since 2015, and conspicuously missing was any reference to “deleveraging”. Investors are interpreting the change in tone as a signal that the government may ease off its tightening measures if warranted.

The Bank of Japan (BOJ) has abandoned its attempt to predict when the island nation would reach 2% inflation, underscoring the difficulty of lifting prices even with Japan’s strengthening economy. The central bank kept its monetary policy unchanged this week and pledged to continue its massive stimulus program until its price goal is obtained. The BOJ introduced massive asset purchases in 2013 aiming to reach the inflation target in around two years. The timeframe was subsequently pushed back six times as slow wage growth and reluctance among consumers to spend kept progress at a lethargic pace.

Finally: Following the financial crisis in 2008, central banks around the world responded by cutting interest rates to 0% or even lower. That resulted in the cry of “TINA, TINA, TINA!” by stock brokers everywhere – “There Is No Alternative” to buying stocks, they cried out.

But times have changed.

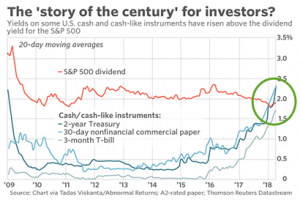

Tadas Viskanta of the financial blog ‘Abnormal Returns’ says the following chart tells “the most important story of the century.” Tadas notes that yields on some U.S. cash and cash-like instruments have now risen above the dividend-yield for the S&P 500. The effect may be that the demand for U.S. stocks will fade as the Federal Reserve continues to hike rates, since, for the first time since 2009, there IS an alternative to stocks.

(sources: all index return data from Yahoo Finance; Reuters, Barron’s, Wall St Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet)

Indices mentioned are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results. All Investing involves risk. Depending on the types of investments, there may be varying degrees of risk. Investors should be prepared to bear loss, including total loss of principal.