3-21-2022 Weekly Market Update

The very Big Picture

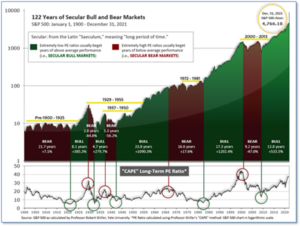

The long-term valuation of the market is commonly measured by the Cyclically Adjusted Price to Earnings ratio, or “CAPE”, which smooths-out shorter-term earnings swings in order to get a longer-term assessment of market valuation. A CAPE level of 30 is considered to be the upper end of the normal range, and the level at which further PE-ratio expansion comes to a halt (meaning that further increases in market prices only occur as a general response to earnings increases, instead of rising “just because”). The market is now above at that level.

Of course, a “mania” could come along and drive prices higher – much higher, even – and for some years to come. Manias occur when valuation no longer seems to matter, and caution is thrown completely to the wind – as buyers rush in to buy first, and ask questions later. Two manias in the last century – the “Roaring Twenties” of the 1920s, and the “Tech Bubble” of the late 1990s – show that the sky is the limit when common sense is overcome by a blind desire to buy. But, of course, the piper must be paid, and the following decade or two were spent in Secular Bear Markets, giving most or all of the mania-gains back.

See Fig. 1 for the 100-year view of Secular Bulls and Bears. The CAPE is now at 36.16, down from the prior week’s 34.31. Since 1881, the average annual return for all ten-year periods that began with a CAPE in this range has been negative (see Fig. 2).

Note: We do not use CAPE as an official input into our methods. However, if history is any guide – and history is typically ‘some’ kind of guide – it’s always good to simply know where we are on the historic continuum, where that may lead, and what sort of expectations one may wish to hold in order to craft an investment strategy that works in any market ‘season’ … whether the current one, or one that may be ‘coming soon’!

The Big Picture:

The ‘big picture’ is the (typically) years-long timeframe – the timeframe in which Cyclical Bulls and Bears operate. The U.S. Bull-Bear Indicator finished the week in Bear territory at 42.70, up from the prior week’s 40.93.

In the Quarterly- and Shorter-term Pictures

The Quarterly-Trend Indicator based on the combination of U.S. and International Equities trend-statuses at the start of each quarter – was Positive entering January, indicating positive prospects for equities in the first quarter of 2021.

Next, the short-term(weeks to months) Indicator for US Equities turned positive on February 28, and ended the week at 25, up strongly from the prior week’s 12.

In the Markets:

U.S. Markets: U.S. stocks moved sharply higher for the week, ending a two-week losing streak and reclaiming much of the ground lost over the past month. Gains were spread across the major indexes, with the tech-heavy Nasdaq Composite staging the biggest rally. The Dow Jones Industrial Average rallied 1,811 points, finishing the week at 34,755—a gain of 5.5%, while the NASDAQ Composite surged 8.2% closing at 13,894. By market cap, the large cap S&P 500 rallied 6.2%, while the mid cap S&P 400 gained 5.3%. The small cap Russell 2000 ended the week up 5.4%.

International Markets: Almost all major international markets finished the week in the green. Canada’s TSX rose 1.7%, while the United Kingdom’s FTSE 100 gained 3.5%. On Europe’s mainland, France’s CAC 40 and Germany’s DAX each rose 5.8%. In Asia, China’s Shanghai Composite ended down -1.8%, but Japan’s Nikkei surged 6.6%. As grouped by Morgan Stanley Capital International, developed markets rallied 7.5% and emerging markets rebounded 6.6%.

Commodities: Major commodities pulled back amid the surge in equity markets. Gold retreated -2.8% to $1929.30 and Silver pulled back -4.1% to $25.09. West Texas Intermediate crude oil fell for a second consecutive week giving up ‑5.7% to $103.09 per barrel, while Brent crude oil ended down -4.2% to $107.93. The industrial metal copper, viewed by some analysts as a barometer of world economic health due to its wide variety of industrial uses, finished the week up 2.5%.

U.S. Economic News: The number of Americans filing first time claims for unemployment benefits dropped to a two-and-a-half month low showing demand for labor remains extremely high. The Labor Department reported initial jobless claims declined by 15,000 to 214,000 last week. Economists had forecast initial jobless claims would total 220,000. Weekly jobless claims now appear on track to approach or even fall below the 200,000 threshold again. They briefly sank to a 52-year low of 188,000 at the end of last year. Meanwhile, the number of people already collecting benefits declined by 71,000 to 1.42 million. That reading is a new post-pandemic low.

The confidence of the nation’s homebuilders pulled back this month, falling to its lowest level since last September. The National Association of Home Builders’ (NAHB) reported its monthly confidence index fell two points to 79 in March. Overall, the index has now declined for four consecutive months, reflecting a multitude of factors currently weighing on the housing market, such as shortages of labor and key raw materials, and now rising interest rates. Nevertheless, scores above 50 indicate that more builders believe that conditions are good rather than poor. Inflation is the primary culprit behind builders’ worsening sentiment. Construction costs have risen over the last 12 months and as the Federal Reserve seeks to ease the run-up in consumer prices, interest rates are rising in response. Economists don’t expect this situation to end anytime soon. Robert Dietz, NAHB chief economist, said in the report, “While low existing inventory and favorable demographics are supporting demand, the impact of elevated inflation and expected higher interest rates suggests caution for the second half of 2022.”

Sales of existing homes pulled back in February according to the latest report from the National Association of Realtors (NAR). The NAR reported existing-home sales decreased -7.2% between January and February, down -2% from the same time last year. Economists had expected an increase in existing-home sales. Lawrence Yun, chief economist for the National Association of Realtors, said in the report, “Housing affordability continues to be a major challenge, as buyers are getting a double whammy: rising mortgage rates and sustained price increases. Some who had previously qualified at a 3% mortgage rate are no longer able to buy at the 4% rate.” Sales declined in every region on a monthly basis, and the South was the only part of the country where February’s sales numbers were higher compared to the previous year. The median sales price for an existing home in February was $357,300, representing a 15% annual increase. But due to rising mortgage rates, monthly payments for newly-purchased existing homes are now 28% higher than they were a year ago, Yun said.

Inflation at the wholesale level surged last month, but there was also some potentially good news. The Labor Department reported its Producer Price Index (PPI) rose a sharp 0.8% in February signaling that the hottest inflation in 40 years is unlikely to cool anytime soon. The increase in wholesale prices over the past year stayed at 10% for the second month in a row—its highest level in decades. However, analysts noted the increase in so-called core wholesale prices rose just 0.2%–its smallest advance in over a year. The core rate excludes the often-volatile, food, energy, and retail trade margins category and is viewed by the Federal Reserve as a better indicator of inflation. Wholesale prices reflect what companies pay for supplies such as grains, fuel, metals, lumber, packaging and so forth. Higher business costs tend to translate into rising prices for customers and more inflation. U.S. economist Mahir Rasheed at Oxford Economics stated, “Inflation in the pipeline is showing few signs of decelerating in the near term, especially as the Russia-Ukraine war wreaks havoc in energy and other commodity markets.”

Sales among the nation’s retailers slowed sharply last month, rising just 0.3% as Americans bought fewer goods amid rising inflation. Economists had expected a 0.4% advance. Retail sales were positive largely because of a 5.3% increase in spending on gasoline, but that reflects rising oil prices and is not good news for either consumers or the economy. Sales for autos and parts also rose 0.8%. Auto sales account for about one-fifth of overall retail spending. If gasoline and autos/parts are excluded, retail sales actually fell -0.4% last month. However, analysts note that Americans still have plenty of savings built up during the pandemic and feel secure in their jobs giving them the confidence to spend. Senior economist Sal Guatieri of BMO Capital Markets wrote in a note to clients, “Though cooling after January’s splurge, American consumers appear reasonably well positioned to keep spending, supported by recent massive job gains and high household savings.”

Manufacturing activity in the New York-area declined this month hitting its lowest level since May of 2020, shortly after the pandemic began. The New York Fed reported its Empire State Business Conditions index plunged 14.9 points to -11.8 in March. The reading missed expectations by a wide margin–economists had expected a reading of 5.5. Readings below 0 indicate deteriorating conditions. Both the new orders and shipments indexes declined in March as businesses reported “ongoing substantial increases” in both input and selling prices. The new-orders index fell 12.6 points to -11.2 in March and the shipments index fell 10.3 points to -7.4. On a positive note, firms were more optimistic about the next six months. The Future Business Conditions index rose 8.4 points to 36.6.

The U.S. Federal Reserve raised its key interest rates for the first time in four years and outlined a more aggressive strategy of “ongoing increases” to fight rising inflation. With inflation running at a 40-year high, the fed raised its benchmark interest rate by a quarter percentage point. The Fed now sees its policy rate hitting 1.9% by the end of the year, jumping to 2.8% in 2023 and 2024. While the quarter point hike was widely expected, the Fed’s long-term estimates were more aggressive than many fed-watchers had expected. Avery Shenfeld of CIBC Economics stated, “The Fed threw down the gauntlet as it confronts a broad inflation upsurge, twinning a widely expected and tame quarter point rate hike with a much sterner message about what lies ahead.” The Fed projected inflation would average 4.3% at the end of 2022, up from its prior 2.6% forecast. The last time the central bank expected inflation to top 3% was in 2007. Fed Chairman Jerome Powell had telegraphed the rate increase earlier this month. There was one dissent, with St. Louis Fed President James Bullard arguing for a 50-basis point rate hike.

International Economic News: A commodities rally sparked by Russia’s invasion of Ukraine will push Canadian inflation higher for longer, the Bank of Canada stated. The central bank now expects the headline rate to peak at or above 6%, forcing the central bank to raise interest rates more aggressively. Canada’s inflation rate has already surged well above the 5.1% that the Bank of Canada forecast for the first quarter in January. A survey of economists at five leading financial institutions and a consultancy showed that most now expect the Bank of Canada to hike borrowing costs four to five times in 2022, lifting its policy rate to 1.25% or 1.5% by the end of the year. Scotiabank is forecasting a year-end policy rate of 2.5%. Canada’s latest inflation data surprised on the upside, with the Consumer Price Index hitting a new 30-year high of 5.7% in February.

It was a similar story across the Atlantic. The Bank of England also raised interest rates this week for a third consecutive time, but struck a more dovish tone when discussing future hikes. The Bank’s Monetary Policy Committee voted 8-1 in favor of a further 0.25 percentage point hike to its main Bank Rate, taking it to 0.75%. U.K. inflation was already running at a 30-year high prior to Russia’s invasion of Ukraine, which sent global energy prices surging. In its report the bank stated, “Global inflationary pressures will strengthen considerably further over coming months, while growth in economies that are net energy importers, including the United Kingdom, is likely to slow.” The BoE is currently forecasting inflation to peak at 8% in the coming months, and perhaps even higher later in the year.

On Europe’s mainland, French President Emmanuel Macron has vowed to intensify his overhaul of France’s welfare state, tax system and labor market if he wins a second term as president next month. Macron stated the transformation of French society would protect people at a time of crisis when the war in Ukraine marked a “return of tragedy in history”. Macron’s poll numbers have risen since Russia’s invasion and is a clear favorite to win April’s election, making him the first French president to win re-election in 20 years. Macron vowed to step up his changes to the welfare state and benefits system, raising the pension age from 62 to 65 and continuing to cut taxes for businesses and households.

Germany’s expectations for economic growth are collapsing, according to the latest data from ZEW (Leibniz Center for European Economic Research). The ZEW Indicator of Economic Sentiment for Germany fell more sharply than ever before in its March 2022 survey. The indicator plunged 93.6 points to -39.3. It was the biggest drop in expectations since the survey began in December 1991. By comparison, the indicator experienced a decline of 58.2 points at the beginning of the COVID-19 pandemic in March 2020. ZEW President Professor Achim Wambach stated, “A recession is becoming more and more likely. The war in Ukraine and the sanctions against Russia are significantly dampening the economic outlook for Germany. The collapsing economic expectations are accompanied by an extreme rise in inflation expectations. The experts therefore expect a stagflation in the coming months.”

In Asia, China’s southern technology hub Shenzhen partially eased its lockdown measures after President Xi Jinping stressed the need to “minimize the impact” of the coronavirus pandemic on the nation’s economy. The city of 17.5 million, under full lockdown since last week, resumed work, factory operations and public transport in four districts and a special economic zone, Shenzhen’s government said. Shenzhen is home to supply chains for major international companies making everything from iPhones to washing machines. Some of China’s biggest tech firms also have campuses around the city. The measures came after Xi referenced the spiraling economic costs of China’s zero-Covid strategy during a Politburo meeting where he vowed to “stick to” the approach, saying “persistence is victory”.

In a sharp contrast to its American and European counterparts, the Bank of Japan struck a dovish stance at its latest policy meeting. The BOJ left its interest rates and asset purchases unchanged, in a move widely expected by economists. With the decision, the BOJ cemented its outlier status following the interest-rate hikes of its global peers this week. While inflation remains subdued in Japan, it is picking up speed. Key consumer prices rose 0.6% last month, according to a government report, as energy costs climbed at the fastest pace in 41 years. Nobuyasu Atago at Ichiyoshi Securities Co. noted the reason for the difference in policy at the BOJ. “The BOJ can’t tighten policy because unlike the U.S. and Europe, domestic demand isn’t driving inflation at all,” he said.

Finally: ‘Help Wanted’ signs are a common sight in towns and cities across the country. According to conventional wisdom, the shortage of workers (aka “missing workers”) is due to older workers, after enjoying outsized gains in their stock portfolios and real-estate holdings, exiting the workforce. However, a deeper look into labor force data from the U.S. Census Bureau shows this isn’t exactly the case. For example, for those ages 62-70, 37.4% were employed in January 2020. That percentage dipped to 30% in April 2020 but rebounded to 36% in January 2022. Similar calculations are done for each age group, shown below. It turns out that the age group contributing most to the “missing workers” total is actually the 15-34 age group. That group alone accounts for 42% of the “missing workers” total. (Chart by Marketwatch.com)

(Sources: All index- and returns-data from Yahoo Finance; news from Reuters, Barron’s, Wall St. Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet.) Securities offered through Registered Representatives of Cambridge Investment Research Inc., a broker-dealer, member FINRA/SIPC. Advisory Services offered through Cambridge Investment Research Advisors, a Registered Investment Adviser. Strategic Investment Partners and Cambridge are not affiliated. Indices mentioned are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results.